What an officially valid document API does for your business

You verify documents from every customer. The process feels rigorous. And fraud still gets through, because human review at volume is structurally unreliable. Here is what an OVD API replaces it with.

Your team collects an official document from every customer at onboarding. Agents check that it looks right, operations cross-references the scan, compliance files it away. The process feels rigorous, and yet document fraud still slips through and audits still turn up gaps. The reason is not weak effort or careless staff. Manual document verification was never designed for digital onboarding at scale, and no amount of optimisation changes that. Adding an OVD API as the document layer of your KYC API integration is not a faster version of the manual process. It replaces visual inspection with database verification, which is structurally more accurate, fraud-resistant, and audit-ready. This guide covers what an OVD API does, where it eliminates risk that manual review cannot, and what to look for in one.

What counts as an officially valid document, and why it matters

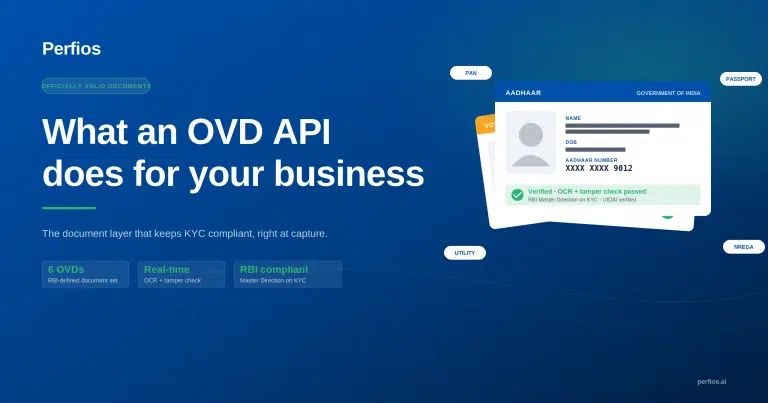

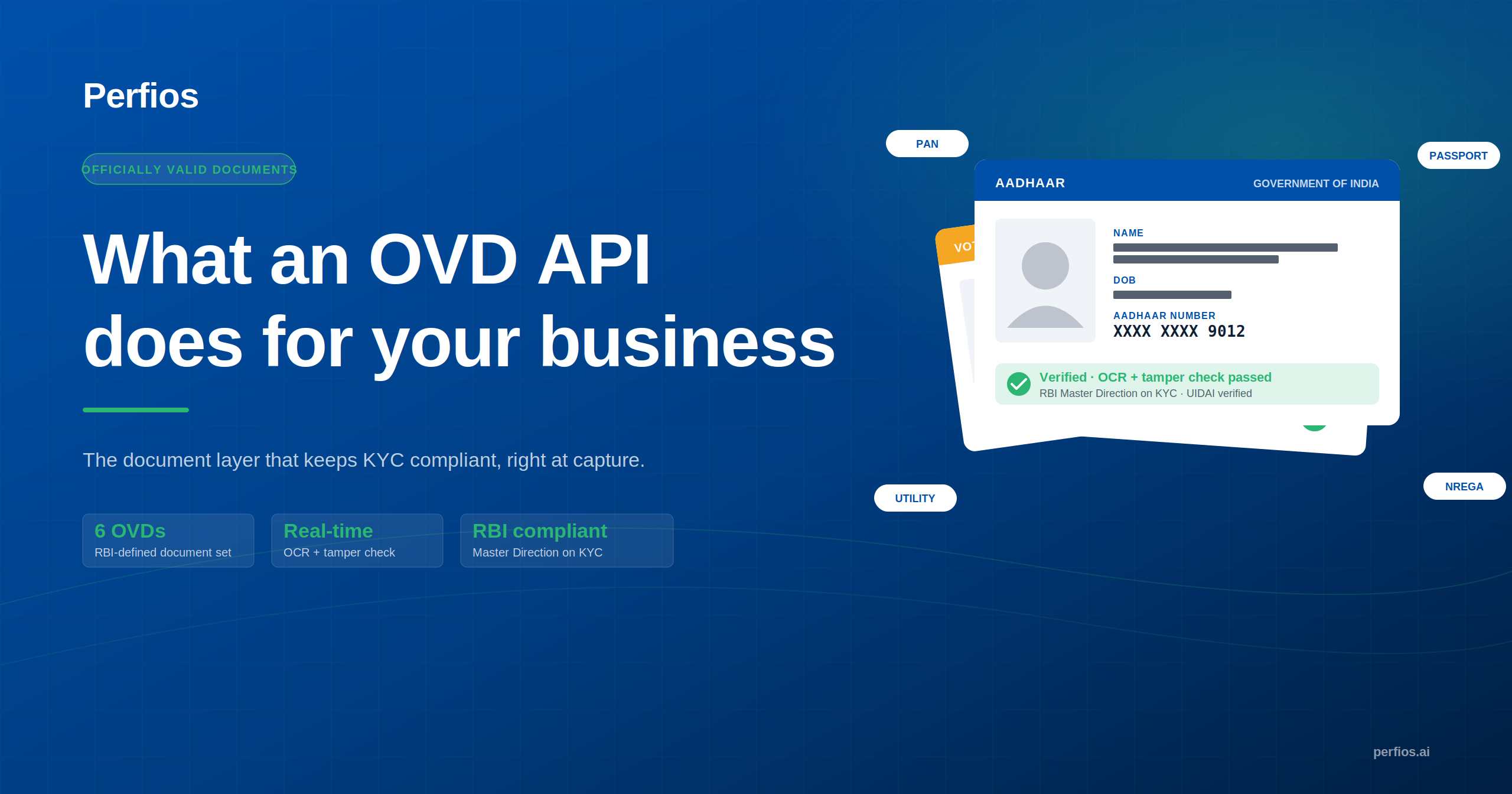

Under RBI’s KYC Directions, six documents qualify as Officially Valid Documents (OVDs): the Passport, Driving Licence, Voter’s Identity Card, PAN Card, Aadhaar, and the NREGA Job Card. Regulated entities, banks, NBFCs, and insurers, must collect and verify one for every customer.

This is regulatory context, not trivia, because getting it wrong carries real consequences. Here are the six, and the one distinction manual review most often misses:

| Document | Proof of Identity | Proof of Address |

|---|---|---|

| Passport | Yes | Yes |

| Driving Licence | Yes | Yes |

| Voter’s Identity Card | Yes | Yes |

| Aadhaar | Yes | Yes |

| NREGA Job Card | Yes | Yes |

| PAN Card | Yes | No |

That last row is the trap. PAN serves as identity proof only. It cannot serve as address proof. A customer who submits PAN without a second document for address is an incomplete KYC, but catching that requires active knowledge of the rule, not a glance at the document. At digital onboarding volumes, a reviewer applying that rule consistently across thousands of files is not a realistic expectation. The API layer exists precisely because database verification is structurally more reliable than visual inspection.

What an OVD API does: four things manual verification cannot

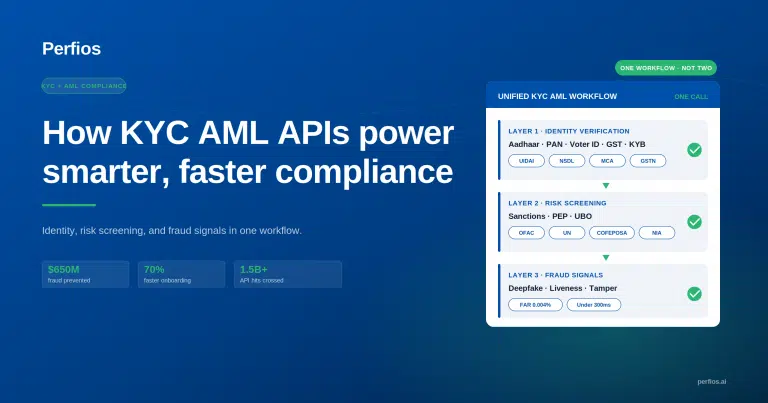

An OVD API is not a faster manual process. It does four things visual review structurally cannot: real-time database verification, OCR extraction that holds at volume, document tamper detection, and automatic audit trail generation.

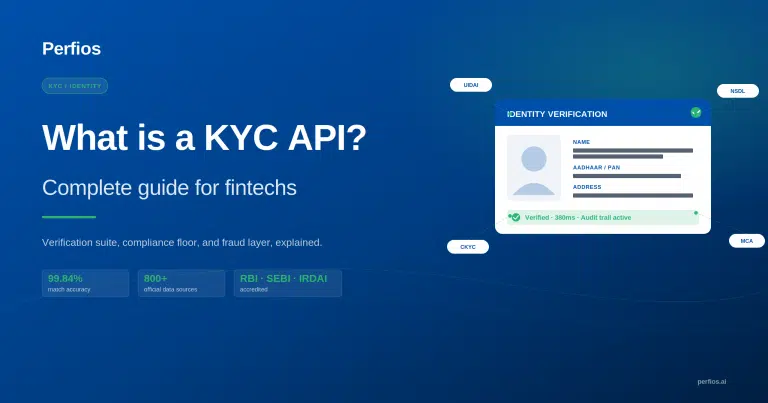

01 Authenticity — Real-time database verification

The API submits document details directly to the authoritative government source, UIDAI for Aadhaar, NSDL for PAN, the Election Commission for Voter ID, and gets back a real-time confirmation. Perfios KYC/KYB does this across 800+ official data sources. A document that looks authentic to a human but contains fabricated details fails immediately at the database layer.

02 Extraction — OCR that does not degrade at volume

The API extracts structured data from document images, including password-protected PDFs. The Perfios OCR API handles popular OVDs this way. Human review accuracy falls as volume rises, API extraction accuracy does not. (For how the extraction itself works, see digitizing documents, the OCR way.)

03 Integrity — Document tamper detection

Visual inspection cannot detect pixel-level alterations, metadata anomalies, or structural inconsistencies in a digitally modified document. Perfios offers Document Tamper and Behavioural Check as a distinct product within its verification suite. This capability has no manual equivalent, there is simply nothing the human eye can do here.

04 Defensibility — Automatic audit trail generation

Every API call produces a timestamped, structured verification record at the point of the call. Under RBI scrutiny, a system-generated audit trail is categorically more defensible than one reconstructed from paper records or an agent’s memory.

Where manual OVD verification breaks down

Manual verification fails in three specific ways at scale: document fraud passes visual inspection, standards drift across branches and agents, and audit records cannot be produced cleanly under regulatory scrutiny.

Failure 1: Document fraud at entry

A tampered document designed to pass visual inspection still fails a real-time database check. Manual review catches appearance. API verification catches authenticity. Those are not the same test.

Failure 2: Inconsistent standards across touchpoints

A business with multiple branches or agents has multiple verification standards in practice, however good the training. An API applies identical logic to every document, every time, regardless of volume or location.

Failure 3: Audit gaps under scrutiny

When a regulator asks for evidence of KYC compliance for a specific customer, a manual process means reconstructing the record from paper and memory. An API-based process produces a complete timestamped record immediately.

70%+

Reduction in onboarding times, Perfios KYC/KYB

~$650M

Fraud prevented at the point of onboarding

800+

Official data sources verified against

What to look for in an OVD verification API

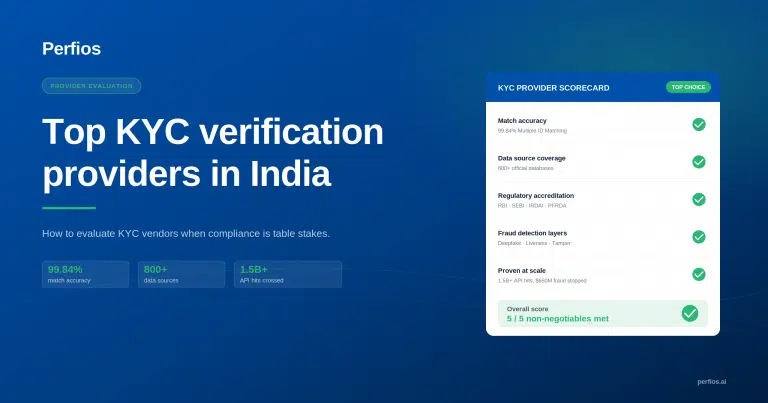

Evaluate an OVD verification API on four criteria: full coverage of all six OVDs, real-time database verification accuracy, tamper detection as a separate capability from OCR, and complete, retrievable audit trails.

| Criterion | What to confirm |

|---|---|

| 1. Document coverage | Does it cover all six RBI-specified OVDs? Partial coverage forces a manual fallback for the rest, which defeats the purpose of automating. |

| 2. Verification accuracy | Real-time database verification is the benchmark. Perfios KYC/KYB achieves 99.84% Multiple ID Matching accuracy across name, date of birth, address, and relative information. |

| 3. Tamper and fraud detection | OCR and database checks confirm the data is real. Tamper detection confirms the document has not been altered. These are separate capabilities, confirm the API includes both. |

| 4. Audit trail completeness | Every call must produce a structured, timestamped record that compliance can retrieve without manual reconstruction. |

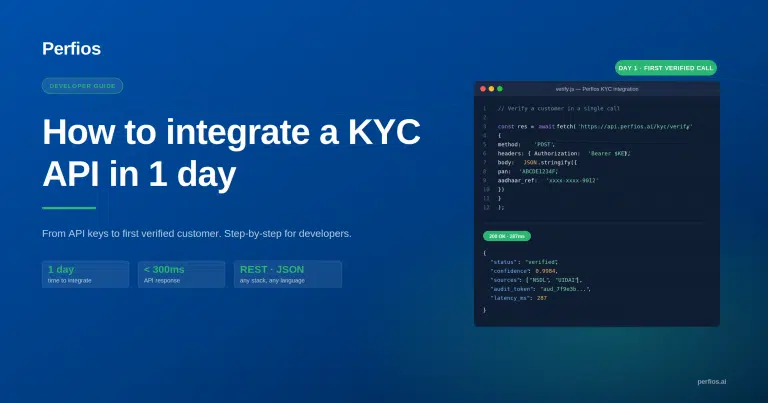

If you are ready to move from evaluating to building, the step-by-step KYC API integration guide walks a developer from the sandbox key to the first verified call.

Verifying OVDs at scale?

See how Perfios KYC/KYB handles OVD verification across 800+ official data sources.

The Takeaway

Manual OVD verification was not poorly designed. It was designed for volumes where individual scrutiny was practical. Digital onboarding at scale made that model obsolete. An OVD API does not speed up the old process, it closes the structural gaps the old process cannot fix at volume: fraud exposure, inconsistency, and audit risk.

You cannot optimise manual verification at scale. You can only replace it.

Frequently asked questions

What is an Officially Valid Document (OVD)?

An Officially Valid Document is a government-issued document that RBI’s KYC Directions accept as proof of identity and, in most cases, address. The six OVDs are the Passport, Driving Licence, Voter’s Identity Card, PAN Card, Aadhaar, and the NREGA Job Card. Regulated entities must collect and verify an OVD for every customer.

What are the six officially valid documents in India?

Under RBI’s KYC Directions the six OVDs are: Passport, Driving Licence, Voter’s Identity Card, PAN Card, Aadhaar, and the NREGA Job Card.

Can PAN be used as address proof?

No. PAN serves as proof of identity only, not address. A customer submitting PAN without a second document for address proof is an incomplete KYC, a distinction that requires active rule knowledge rather than visual inspection.

What does an OVD API do?

An OVD API verifies official documents in real time against authoritative government sources, extracts structured data through OCR, detects tampering that visual inspection cannot, and generates a timestamped audit trail on every call. It replaces manual document review rather than speeding it up.