What is a KYC API? The complete guide for fintechs

Whether you are researching KYC APIs for the first time, comparing providers, or already integrated and hitting walls at scale, the same question decides the outcome. Here is what it is, and how to choose an API that holds up.

You have probably arrived here in one of three states. You are researching KYC APIs for the first time and want a clear picture before you commit. You are comparing providers and trying to work out what actually separates one from another. Or you already integrated a KYC API months ago, onboarding got faster, the last audit passed, and yet things still break at scale: verifications time out at peak load, a tampered document slips past the OCR, the compliance team asks again for cleaner logs.

All three roads lead to the same fork. The teams whose onboarding holds up and the teams whose onboarding breaks usually made one decision differently and early: whether to treat a KYC verification API as a compliance checkbox or as infrastructure. This guide covers what a KYC API actually does, why the cheapest integration so often becomes the most expensive one, and the five criteria that separate a point solution from a verification platform you can build a business on. If you are new to the topic, start at the top. If you are evaluating vendors, the 5-point framework near the end is the part to bookmark.

What is a KYC API, and why most teams integrate it wrong

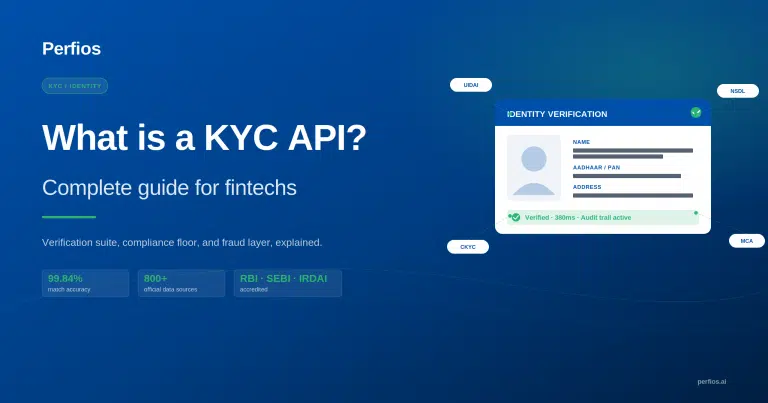

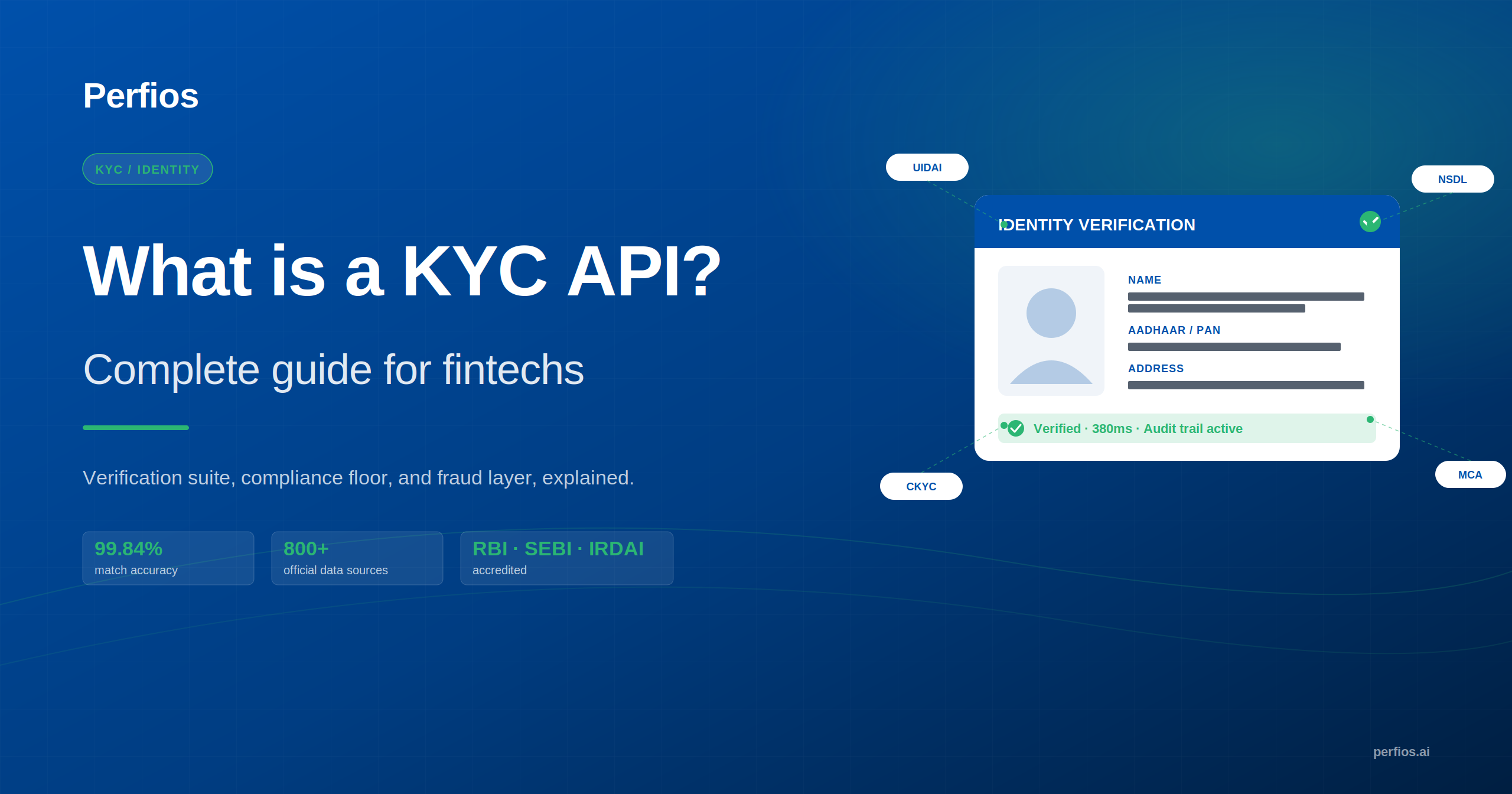

A KYC API is an endpoint that verifies a customer’s identity in real time against authoritative databases such as UIDAI and NSDL, returning a structured pass, fail, or review decision in seconds. The mistake is treating that single decision as the entire job, when it is only the floor.

Picture the team that shipped fast. They wired up a free KYC verification API for ID checks, cleared the regulator’s onboarding requirement, and moved on to the next sprint. Six months later, a fraud ring onboards using lightly edited PAN images that the OCR reads as clean. The accounts pass KYC, transact, and disappear. The integration did exactly what it was asked to do. It was never asked to detect fraud.

That is the pattern. A compliance-first integration optimises for one question, “will this satisfy the regulator,” and silently ignores the questions that decide whether the business survives contact with real users: does it hold up under load, does it catch manipulation, does it produce an audit trail anyone can defend a year later.

Here is the reframe worth internalising before reading another vendor page. Compliance is the floor, not the ceiling. The fintechs winning on customer acquisition do not treat KYC as a gate they grudgingly install. They treat it as a conversion lever (fewer drop-offs from failed checks) and as a fraud layer (fewer losses from identities that should never have passed). Same API call, entirely different mandate.

How a KYC verification API works, from single endpoint to full suite

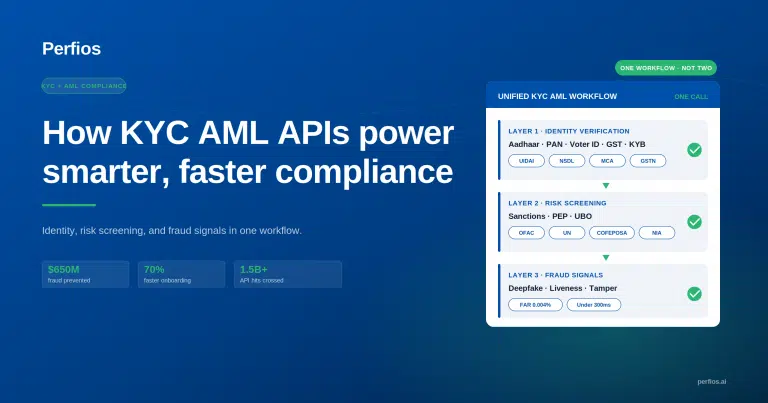

A KYC verification API follows a simple lifecycle: your system sends a request, the API queries the relevant database in real time, it scores the match, and it returns a structured response. The scope of what it can check is what separates a basic endpoint from a verification suite.

The lifecycle is the easy part. The depth is where the real difference lives. A single-endpoint mindset, “we verify PAN, we are done,” is structurally inadequate for a product that touches money, because identity is rarely established by one document. A modern KYC API suite spans several verification types:

- Identity: Aadhaar, PAN, Voter ID and Passport checks against the source database.

- Address: Validation and standardisation of declared addresses.

- Professional credentials: Confirming a stated role or registration.

- Bank account: Ownership and validity (covered in depth in our bank verification API guide, referenced here, not repeated).

- Business and GST: For KYB and merchant onboarding.

- OCR extraction: Pulling fields off a document image so a human never rekeys them.

- Liveness and anti-spoof: Confirming a real person is present, not a photo of a photo.

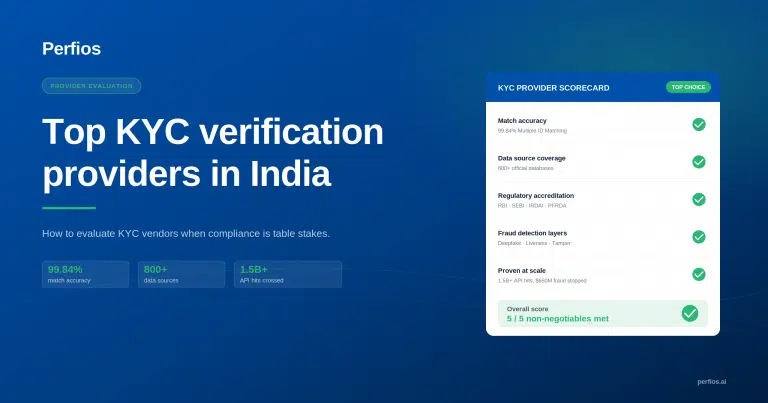

Two endpoints can both claim to “verify identity” and perform completely differently, because the variable that matters is accuracy at the matching layer, not the existence of the call. A noisy matcher either waves through mismatches or rejects legitimate customers, and both failures cost money. Perfios reports 99.84% accuracy on multiple ID matching—the kind of benchmarked figure worth asking every vendor to put in writing.

Why “free KYC verification API” is the wrong search

A free KYC verification API is genuinely useful for early-stage testing. The trouble is that “free vs. paid” is the wrong axis. The real question, once you are processing real volume, is point solution vs. platform, and the cost you are not seeing is the cost of everything the free tier leaves out.

This is not a pitch to ignore cost. Free and low-cost tiers exist for good reasons. If you are validating a flow, building a proof of concept, or onboarding your first few hundred users, a free KYC verification API is a sensible place to start. Searching for one is a reasonable thing to do.

The problem is what the search quietly assumes: that the meaningful difference between providers is the per-call price. At scale, that is the smallest line in the total. Here is what tends to be missing from the free tier, and what each gap costs later:

| What free tiers omit | What it costs at scale |

|---|---|

| Rate limits suited to testing, not production | Verifications fail exactly when traffic peaks |

| No SLA | No recourse, and no uptime guarantee, when it breaks |

| Limited document and ID types | Whole customer segments cannot onboard |

| No audit trail | The compliance ask you cannot answer next quarter |

| No liveness or anti-spoof | Static checks a determined fraudster walks past |

The question was never free versus paid. It is a point solution versus platform, and a fraud loss erases a year of per-call savings in a single afternoon.

What your KYC API must handle on compliance

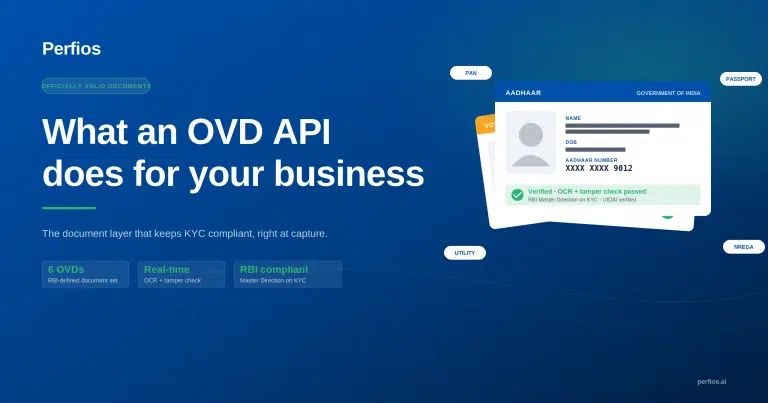

Compliance is table stakes, not a differentiator. A KYC API operating in India has to handle the RBI’s KYC Master Directions, UIDAI requirements, the CKYC registry, and PMLA obligations as a baseline, and it has to do so without becoming the reason you fail an audit.

The regulatory landscape is non-negotiable, so the goal is not to admire it but to clear it cleanly. In practice, a compliant API should handle four things by default rather than as add-ons: zero data storage where the regulation requires it, audit trail generation on every transaction, video KYC (VKYC) for remote onboarding, and consent management so you can prove a customer agreed to what you collected.

On the proof points that matter for diligence, Perfios is built to operate inside this landscape rather than around it:

- Accredited across India’s major financial regulators: the RBI, SEBI, IRDAI, and PFRDA.

- CKYC is handled through a single API call (the mechanics, including KIN issuance and the RBI amendment, are covered in our CKYC guide).

- Video PD (VKYC) with 50+ configurations for different onboarding journeys.

- Zero data storage on Aadhaar verification (see the Aadhaar verification API for the UIDAI-specific detail).

And here is the pivot that the rest of this guide turns on: compliance coverage means nothing if the API fails at fraud detection. Passing an audit and stopping a fraud ring are different tests, and only one of them shows up on your loss statement.

When a KYC API becomes your fraud layer

A KYC API built correctly is your fraud prevention layer, not a bolt-on you add later. Identity verification and fraud detection are the same workflow viewed from two angles, and the gaps a basic API leaves open are exactly the gaps fraudsters are built to exploit.

Fraud arrives in two broad shapes, and a basic identity match misses both:

- Document fraud: OCR alone reads a document; it does not interrogate it. A digitally altered ID, a recycled template, or a synthetic document can extract cleanly and still be fake. Closing the gap takes document tamper detection, deepfake detection for manipulated media, and behavioural checks that flag patterns a single image cannot reveal.

- Identity fraud: A static ID check confirms a document exists. It does not confirm a real, live person is presenting it. Liveness detection and anti-spoof checks address what static verification leaves open: the photo-of-a-photo, the replayed video, the mask.

The fraud stack in practice: Perfios closes these gaps with TrustArmour, Liveness Detection, and Document Tamper and Behavioural Check, with Deepfake Detection layered in for manipulated media. The forward edge of this is KSCAN AI, conversational KYC and KYB workflows that move verification from a form into a guided exchange.

When these layers sit inside the same API that handles identity, fraud prevention stops being a separate project with its own integration, its own vendor, and its own blind spots between the two. It becomes a property of onboarding itself.

How to evaluate a KYC verification API: a 5-point framework

Evaluate any KYC verification API on five criteria: benchmarked accuracy, coverage, latency under peak load, compliance fit for your specific regulator, and fraud layers beyond a basic identity match. If a vendor cannot give you a straight answer on all five, you have your answer.

99.84%

Multiple ID matching accuracy, Perfios benchmark

50+

VKYC configurations for remote onboarding

4

Regulators accredited: RBI, SEBI, IRDAI, PFRDA

| Criterion | The question to ask |

|---|---|

| 1. Accuracy rate | Is it benchmarked and stated in writing, or self-reported and vague? |

| 2. Coverage | Which ID types, databases, and geographies, and do they match your customers? |

| 3. Latency SLA | What is the guaranteed response time, and how does it behave at peak load? |

| 4. Compliance coverage | Does it cover your specific regulator’s requirements, not a generic checklist? |

| 5. Fraud layers | What sits beyond the identity match, liveness, tamper, deepfake, behavioural? |

Run any provider through these five and the point-solution APIs separate from the platforms quickly. The cheap endpoint answers one of the five. A verification platform answers all five with the same contract, the same logs, and the same team behind it when something breaks at 2 a.m.

The Takeaway

A KYC verification API is not a compliance toggle you switch on and forget. It is the architectural foundation for three things at once: fraud prevention, customer conversion, and regulatory resilience. The teams whose onboarding breaks at scale almost always made the same early call, choosing a point solution for a job that needed a platform. The fix is rarely a better integration. It is a better question: not “what is the cheapest API that passes the audit,” but “what verifies identity, stops fraud, and holds up under load on one contract.”

Evaluating KYC API providers?

See how Perfios handles identity, compliance, and fraud on a single platform, KYC and KYB built for scale.

See how Perfios KYC/KYB works →

Frequently asked questions

What is a KYC API?

A KYC API is an endpoint that verifies a customer’s identity in real time against authoritative databases such as UIDAI and NSDL. It lets a fintech confirm who a customer is during onboarding, returning a structured pass, fail, or review decision in seconds instead of through manual document checks.

Is there a free KYC verification API?

Yes, searchers looking for a kyc verification api free option or testing tier will find useful sandboxes. They typically come with rate limits, no SLA, limited document types, no liveness or anti-spoof checks, and thin audit logging, which is why most teams outgrow them once onboarding volume rises.

What is the difference between a KYC API and a KYC platform?

A KYC API is a single verification endpoint. A KYC platform combines identity, address, bank, business, and document checks with fraud layers, compliance tooling, and audit trails behind a unified contract, so the decision logic scales as products and regulators change.

How do I evaluate a KYC verification API?

Evaluate on five points: benchmarked accuracy rate, coverage of ID types and geographies, latency SLA under peak load, compliance coverage for your specific regulator, and fraud layers beyond a basic identity match.