Every credible lender now has AI-powered bank statement analysis. Sub-minute parsing. 99%+ accuracy. Hundreds of bank formats. The capability that defined fintech credit infrastructure five years ago is now table stakes.

So why are most lenders still losing the same fraud cases, missing the same income signals, and approving the same risky borrowers they were five years ago?

Looking across 1,000+ financial institutions in 20+ countries, the answer is clear: the advantage has moved. Reading the statement is no longer the work. The real work is reading across statements, between documents, and into the next step of the credit decision. The institutions that have figured that out are pulling ahead. The ones that haven’t are running a race that has already ended.

Why the category just matured

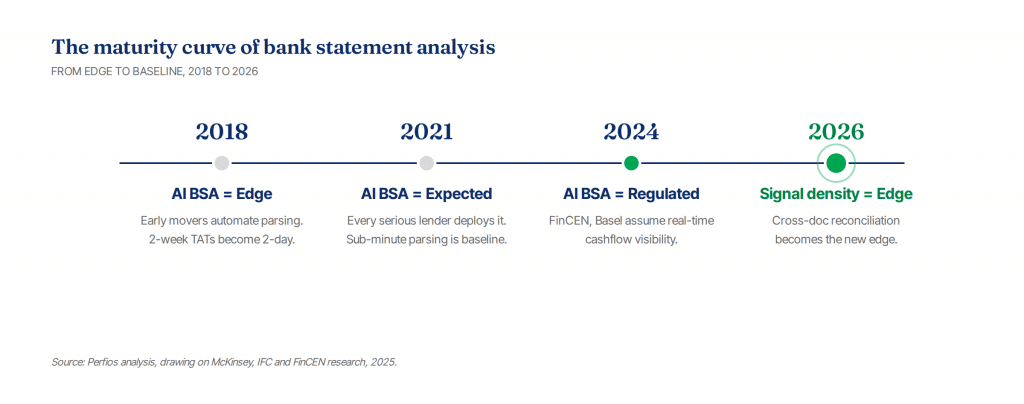

Three forces converged in the last sixty months and pushed BSA from a category-defining capability into commodity infrastructure. The shift is permanent.

First, the OCR ceiling has been reached. Best-in-class extraction is consistently above 99% on mainstream bank formats. No underwriter’s loss curve is shaped by going from 99.3% to 99.7%.

Second, speed is no longer scarce. Sub-minute parsing is the industry baseline. McKinsey research on European SME lending found top banks already delivering instant decisions for simple cases, full underwriting in days, not weeks.

Third, regulators have caught up. FinCEN’s 2024 alert called out AI-generated bank statements explicitly. Basel guidance increasingly assumes real-time cashflow visibility. Whatever you call your BSA program, the regulator now expects you to have one.

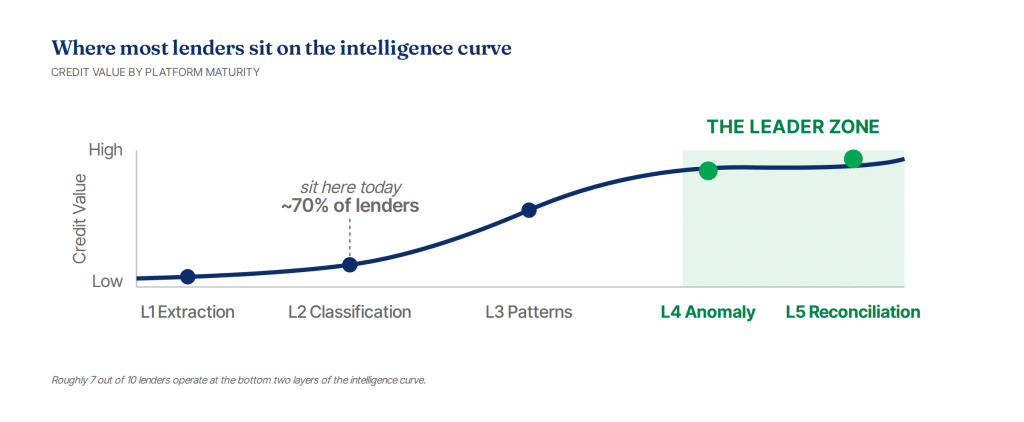

The five layers of bank statement intelligence

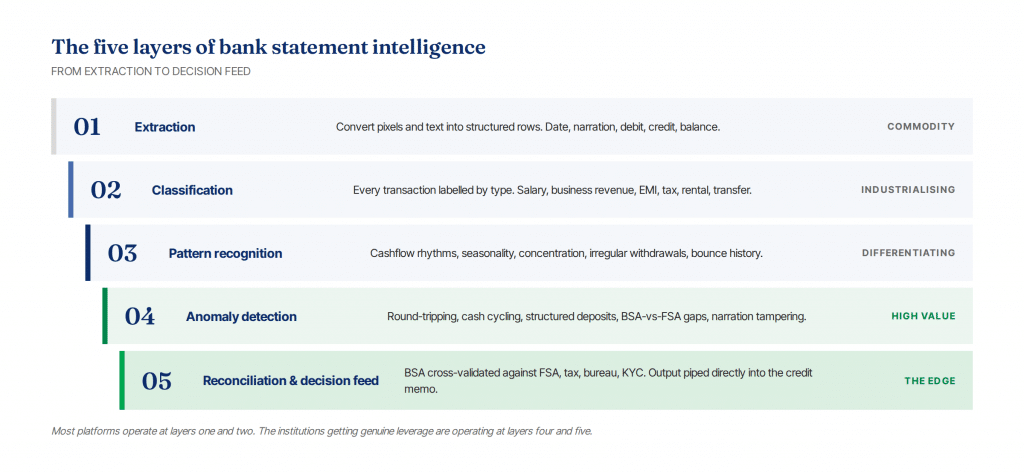

Not all BSA platforms are doing the same work. Five distinct layers of intelligence sit between a raw PDF and a credit decision. The further down the ladder a platform operates, the higher the value it creates – and the harder it is to replicate.

The first two layers – extraction and classification – are now commodity. Pixels become rows. Rows get labelled: salary, EMI, rental, tax, transfer. Any credible platform does this in seconds, at 99%+ accuracy. Roughly 7 out of 10 platforms operate here.

Layer three is pattern recognition: cashflow rhythms, seasonality, counterparty concentration, irregular withdrawals, bounce history. This is where the statement starts to tell a story rather than report a list of transactions.

Layer four is anomaly detection: round-tripping, cash cycling, structured deposits, BSA-versus-FSA gaps, narration tampering. Signals that no single statement reveals on its own.

Layer five is reconciliation and decision feed. BSA cross-validated against tax filings, bureau records, KYC. The output isn’t a report – it’s a populated section of a credit memo, a triggered policy check. This is where the edge lives.

Where the new edge lives

If extraction and speed are no longer differentiators, three capabilities are. None is about reading the statement faster. All of them are about reading across documents, between them, and into the next step of the credit workflow.

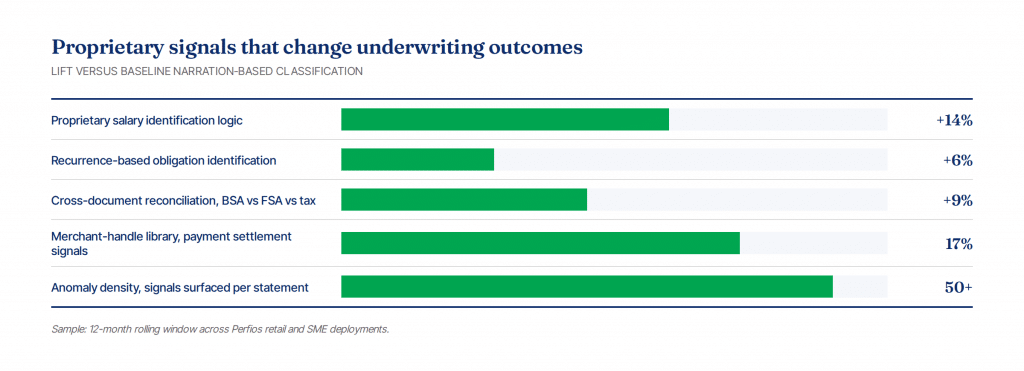

Signal density. Leading platforms surface 50+ fraud and risk signals per statement – round-tripping, cash cycling, structured deposits, narration tampering, counterparty concentration. Most platforms surface fewer than 10. That gap doesn’t show up in your demo. It shows up in your loss curve, six months later.

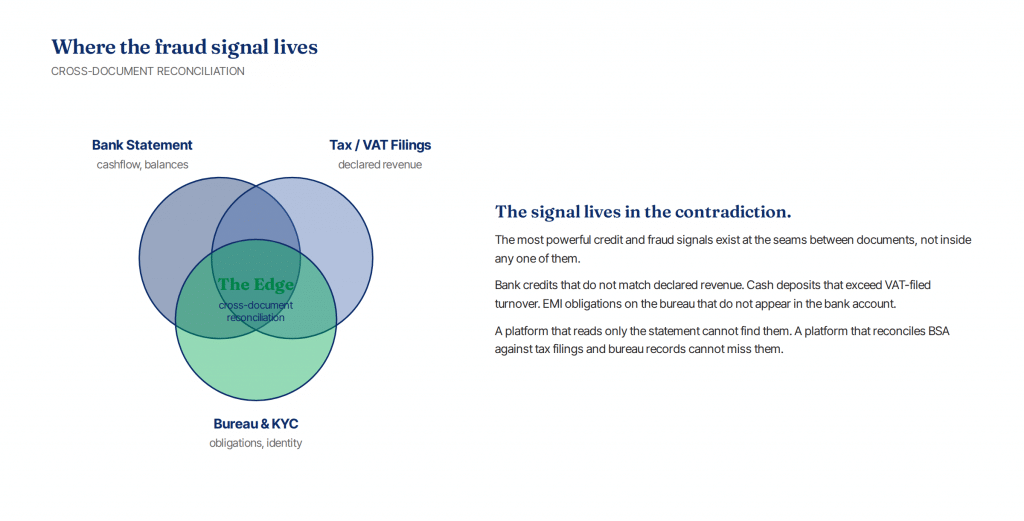

Cross-document reconciliation. The hardest fraud signals to fake are the ones that require coordination across documents. A fraudster can fabricate one credible bank statement. Producing one that also reconciles to a manipulated tax filing, financial statement, and bureau record is exponentially harder. Reconciliation isn’t a feature. It’s where the edge lives.

Decision integration. The end state of a BSA platform shouldn’t be a report. It should be a populated section of a credit memo, a triggered policy check, a routed application, a flagged exception. A 98%-accurate BSA wired into the credit memo creates more value than a 99.5%-accurate one that produces an Excel for a human to re-key.

What good looks like in deployment

Watching dozens of institutional deployments across emerging and developed markets, the pattern is consistent enough to describe as a playbook. Lenders that get real leverage do five things in roughly the same order.

They start with the credit policy, not the technology. They rewrite the policy to take advantage of signals underwriters previously didn’t have. A state-of-the-art BSA wired to an unchanged policy delivers marginal value.

They integrate at the LOS, not the inbox. The platforms that get used disappear into the loan-origination system. The ones that get bypassed ask underwriters to log into a separate portal.

They reconcile, not just analyse. Deployments that move the loss curve wire BSA into a triangle with the financial statement and tax filing. The signal that catches revenue suppression lives in the gap between three documents.

They expand the credit box, not shrink it. The institutions seeing double-digit growth use BSA to lend to borrowers the bureau couldn’t assess – thin-file SMEs, first-time borrowers, the informal economy.

They monitor, not just originate. The richest data on a borrower is not at the application. It’s in the twelve months that follow. Quarterly re-ingestion catches stress before it becomes default.

What we see from inside the data

We process roughly 75 million statements a year on behalf of more than 1,000 financial institutions across 20+ countries. The view from inside that data shapes everything in this thesis. A few proprietary signals are worth singling out – the kinds of signals that materially change underwriting outcomes and that most general-purpose BSA tools cannot replicate.

Two patterns we see that the research record doesn’t yet capture:

The fraud surface is moving from documents to coordination. Single-document attacks like tampered narrations are easier to catch at the document layer. The faster-growing pattern is coordinated synthetic identities applying across multiple institutions – documents internally consistent but inconsistent with each other and with public records. The defence is network-level, not pixel-level.

The bottleneck has moved upstream. In most emerging markets, the constraint on lending is no longer the underwriting decision itself. It’s the data infrastructure that feeds it – account aggregation, e-invoicing, tax data access, KYC utilities. Where this infrastructure exists, AI-powered underwriting is transformative. Where it doesn’t, even the best platform is solving a smaller problem.

The bottom line

The institutions that will define lending in the next decade aren’t the ones that adopted BSA earliest. They’re the ones that built, on top of it, a decision engine that thinks across documents, learns from every file, and disappears into the workflow.

Reading the bank statement is no longer the work. Reading across statements is. The leaders have already moved. The question for every other institution is how long they wait to follow.