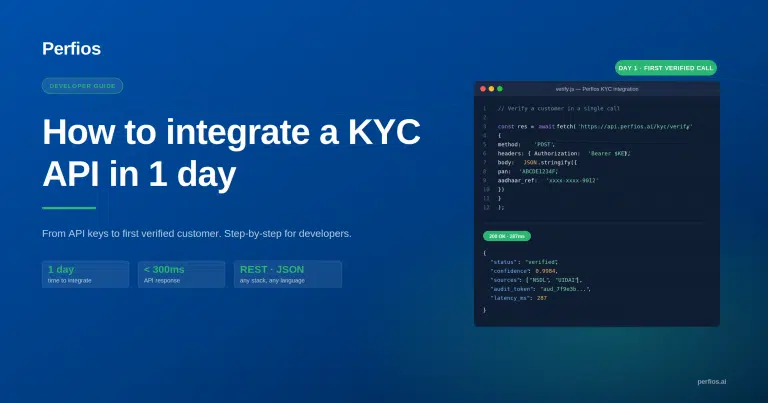

How KYC AML APIs power smarter, faster compliance

KYC and AML are not two separate tools. A unified KYC AML API closes the compliance gaps that siloed systems leave behind, by handling identity verification and risk screening in one workflow instead of in sequence.

A customer clears KYC on Tuesday. Identity verified, documents matched, onboarding complete. On Thursday, your AML screening runs and flags the same customer on a sanctions list. They are already inside, already transacting. Now the cost is not prevention, it is remediation: regulatory exposure, reputational risk, and operational rework to unwind an onboarding that should never have finished. The instinct is to blame the AML tool for being slow. The real cause sits one level deeper. KYC and AML were built as separate compliance disciplines, and most KYC AML API stacks still treat them that way. That gap between identity and risk is not a data problem you can patch. It is an architecture problem. This guide covers what a unified KYC AML API actually does, where it closes risk that siloed stacks cannot, and what to evaluate when choosing one.

Why KYC and AML were never meant to run in sequence

KYC and AML answer two different questions about the same customer, and they were always meant to inform each other. Running them in sequence is not a workflow inefficiency, it is a structural failure that hides risk until after onboarding is done.

KYC answers one question: is this person who they claim to be? AML answers a different one: does this person pose a risk to the financial system? A clean identity match tells you nothing about sanctions exposure, and a sanctions screen assumes an identity you have already established. The two were designed to work together. Legacy technology, separate vendors, separate teams, separate databases, is what pulled them apart.

So consider what the gap actually produces. A customer who clears identity verification but appears on a sanctions list is not a KYC failure. The identity check did its job. It is an AML failure that a fragmented stack made invisible until onboarding was already complete. The tools both worked. The sequence between them is what broke.

India’s regulatory intent points the same way. Under the PMLA, customer due diligence is framed as a continuous process, not a two-step one, identity and risk are meant to be assessed together and on an ongoing basis. The regulation already assumes unification. It is the technology architecture that lags, and a unified AML KYC API closes that gap by design, handling identity and risk screening in the same platform workflow rather than in sequence.

Sequential: KYC then AML

Unified: one workflow

Sequential stacks leave a window between identity clearing and risk screening. A unified workflow removes it.

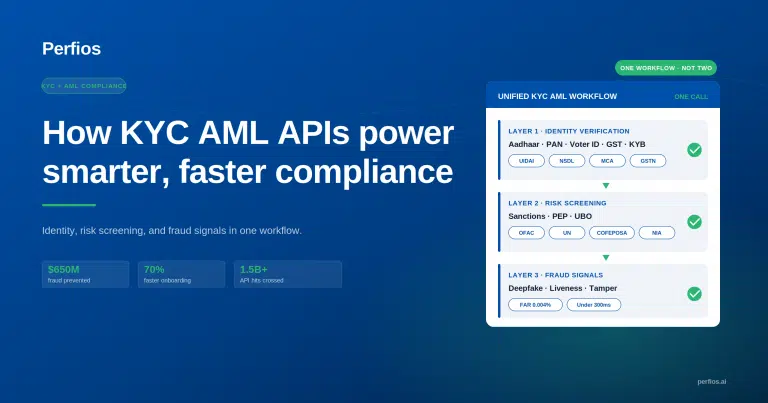

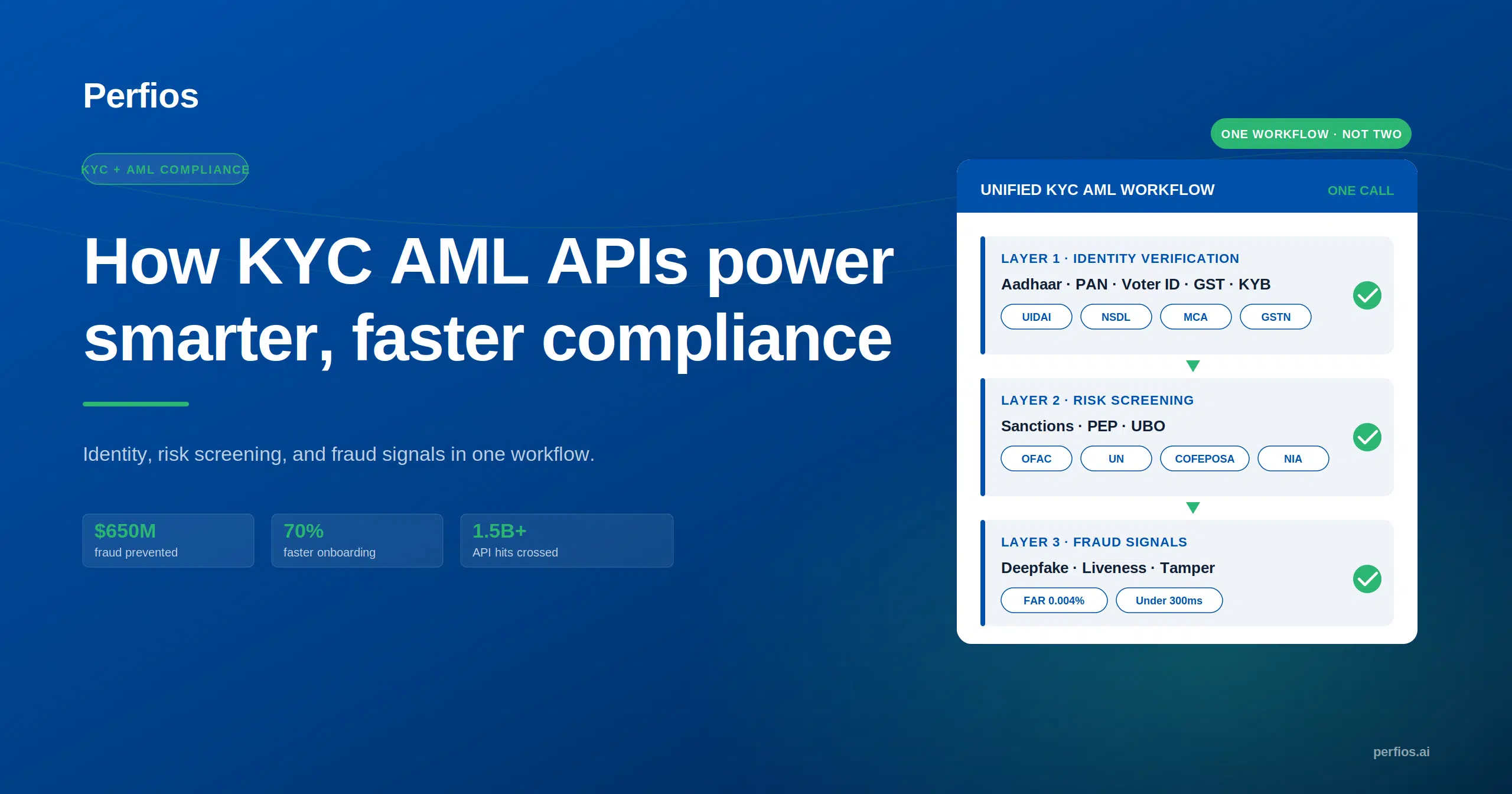

What a KYC AML API does: three layers, one workflow

A unified KYC AML API runs three layers inside a single workflow: identity verification, risk screening, and fraud signal detection. The customer is verified, screened, and fraud-checked in one platform before onboarding completes, not across separate systems with gaps between them.

Layer 1: Identity verification

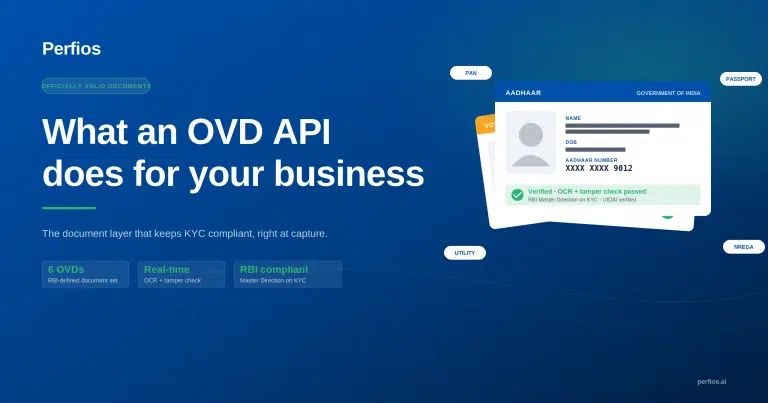

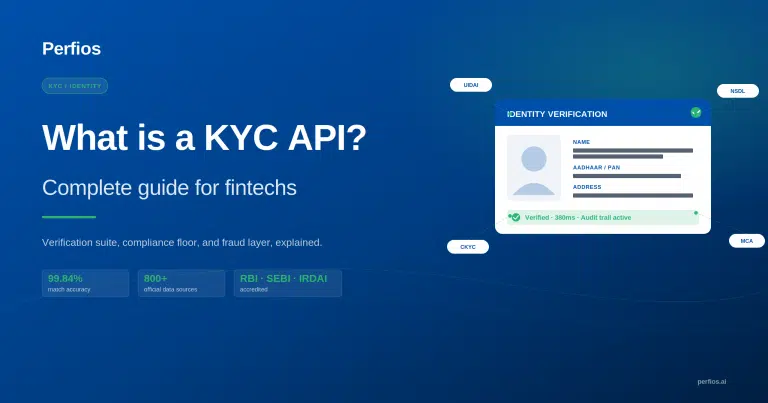

Real-time verification against government databases, Aadhaar, PAN, Voter ID, GST, professional credentials, vehicle ownership, and utility bills. Perfios KYC/KYB runs this across 800+ official data sources at 99.84% Multiple ID Matching accuracy, with AI-powered auto-correct for Indian name and address quirks such as regional prefixes and suffixes, missing spaces, and phonetic variations.

Layer 2: Risk screening

Sanctions and PEP screening combined with identity in one platform, not bolted on afterwards. Perfios Compliance Check screens against OFAC, INTERPOL, UN, COFEPOSA, NIA, Australia, and UK sanctions lists, identifies PEPs by PAN, name, and other parameters, and runs UBO verification covering shareholding pattern, CIN, DIN, related parties, and associated PEPs.

Layer 3: Fraud signal detection

The layer most stacks treat as a separate product: document tamper detection, deepfake detection, liveness checks, and anti-spoof verification. Perfios Deepfake Detection operates at a 0.004% false acceptance rate, with analysis completing in under 300ms.

The outcome is the point. When all three layers sit in one workflow, a customer is verified, screened, and fraud-checked before onboarding completes. There is no handoff between systems for risk to slip through, because there is no handoff.

The three compliance gaps siloed stacks leave open

Running KYC and AML separately produces three specific failure modes: a timing window before risk screening completes, a split audit trail across two systems, and a blind spot for PEP associates and beneficial owners. Each is a direct consequence of the architecture, not the tools.

Gap 1: The timing window

Identity clears. AML has not run yet. The customer is onboarded before risk screening completes, and the sanctions flag arrives after they are already inside. A platform that combines both eliminates this window by design.

Gap 2: The split audit trail

KYC logs live in one system, AML logs in another. Regulators expect a single continuous audit trail per customer. Reconciling two systems under audit pressure is exactly where compliance teams lose time they do not have.

Gap 3: The PEP and UBO blind spot

A customer who is not personally on a sanctions list, but is a close associate of a politically exposed person or controls a beneficial ownership structure, clears basic KYC cleanly. Screening associates and beneficial owners needs a dedicated data layer that siloed KYC stacks do not include by default. For the depth this requires, see our guide on handling politically exposed persons in KYC compliance.

What unified looks like in practice

The three-layer model is not theoretical. Perfios runs identity, risk, and fraud screening through combined products, Compliance Check and OneSDK, with platform results to match.

Perfios Compliance Check screens against OFAC, INTERPOL, UN, COFEPOSA, NIA, Australia, and UK sanctions lists, identifies PEPs by PAN, name, and additional parameters, and verifies UBOs across shareholding pattern, CIN, DIN, related parties, and associated PEPs. (Source: perfios.ai/in/products/compliance-check)

Perfios OneSDK centralises onboarding by combining ID verification, biometrics, and AML screening in a single SDK, the unified architecture in one integration rather than three. (Source: perfios.ai/in/products/onesdk)

70%+

Reduction in onboarding times

~$650M

Fraud prevented at point of onboarding

1.5B

API hits crossed in 2023

Platform figures from perfios.ai/in/products/kyc-kyb.

See the unified model in action

Compliance Check and OneSDK handle identity and AML screening in one combined workflow.

See how Compliance Check and OneSDK work together →

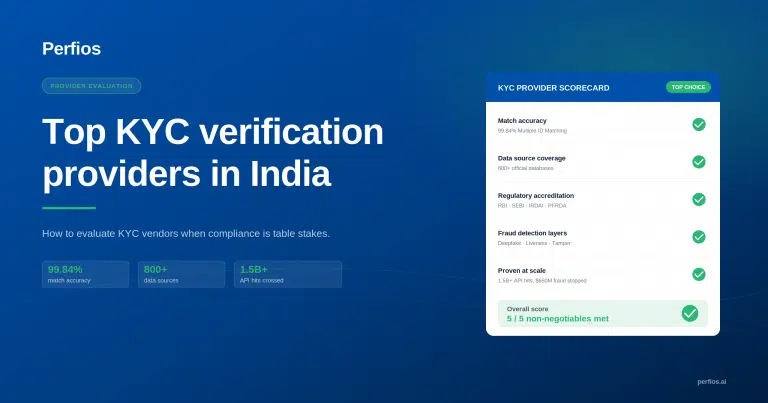

What to evaluate in a KYC AML API: four non-negotiables

When comparing KYC AML APIs, four criteria validate whether the architecture is genuinely unified: combined rather than sequential screening, sanctions list depth including domestic lists, PEP and UBO coverage, and a single audit trail.

| Criterion | The question to ask |

|---|---|

| Combined, not sequential | Does the platform run identity verification and sanctions screening in one workflow, or does one trigger the other after it completes? Sequential is the flaw this guide diagnosed. |

| Sanctions list depth | OFAC and UN are the floor. India-regulated businesses also need COFEPOSA and NIA coverage. Missing domestic lists is a material compliance gap. |

| PEP and UBO depth | Does it screen close associates and beneficial owners, not just the named applicant? A PEP check that stops at the individual misses the most common evasion structure. |

| Single audit trail | Does it produce one regulator-ready record across both identity and AML checks? Separate logs mean reconciliation work at the worst possible moment. |

The Takeaway

The compliance gap between KYC and AML is not a technology problem waiting to be solved. It is an architecture choice that most stacks still make wrong. Organisations that close it are not doing more compliance. They are doing compliance at the only moment it matters: before onboarding completes, not after.

The problem was never the tools. It was the gap between them.

Frequently asked questions

What is a KYC AML API?

A KYC AML API combines identity verification (KYC) and anti-money-laundering risk screening (AML) in a single workflow rather than running them as two separate steps. It verifies who a customer is and screens them against sanctions and PEP lists in the same platform, before onboarding completes.

What is the difference between KYC and AML?

KYC answers whether a person is who they claim to be through identity verification. AML answers whether that person poses a risk to the financial system through sanctions, PEP, and beneficial-ownership screening. They are meant to inform each other, which is why running them in sequence leaves gaps.

Why should KYC and AML run in one workflow?

Running them sequentially creates a timing window where a customer can clear identity verification and be onboarded before AML screening completes, then surface on a sanctions list afterwards. A unified KYC AML API removes that window, produces one audit trail, and screens beneficial owners and PEP associates that basic KYC misses.

What should I evaluate in a KYC AML API?

Four things: whether identity and sanctions screening run in one combined workflow rather than in sequence, sanctions list depth including domestic Indian lists like COFEPOSA and NIA, PEP and UBO screening that covers associates and beneficial owners, and a single regulator-ready audit trail across both checks.