Introduction:

The customer onboarding process is changing in a big way as lending changes all the time. As banks and other financial institutions deal with the difficulties of meeting regulations, managing risk, and meeting customer expectations, the need for new ideas has never been greater. Digital transformation is at the heart of this change. By using digital validations and API-first stacks, institutions can make fewer mistakes and speed up the onboarding process with ease.

By using the latest technologies and putting digital first, businesses can make their operations more efficient, improve their ability to manage risk, and give customers a smooth experience. This big change will help every step of the lending process, from the first lead entry to the last fund disbursement. Digital transformation also promises better security, which is very important in a time when cyber threats and data breaches are on the rise. Institutions can protect sensitive customer information and lower the risk of fraud by using strong security measures and cutting-edge encryption technologies.

Understanding Lending Onboarding Journeys:

The onboarding journey is at the heart of every lending institution. It includes steps like creating leads, processing applications, verifying information, and giving permission. At every step, you need to pay close attention to the details to make sure you follow the rules and lower the risks as much as possible. By understanding the subtleties of these stages, organisations can make their onboarding processes more efficient and faster.

The specific stages include but are not limited to:

● Initial lead creation

● Application creation

● Identify and KYC verifications/validations

● Income & Employment verifications/validations

● Loan purpose-related checks

● Credit risk and Fraud risk due diligence

● Documentation due diligence

● Execution of applications like agreements, contracts, terms & conditions, collection of charges

● Sanction

● Post-sanction due diligence

● Repayments mandate setup

● Disbursement

Gone are the days when customer onboarding was limited to traditional channels. Today, institutions must cater to diverse sourcing points, including direct-to-customer, relationship manager-led, and channel partner-led journeys. Moreover, the advent of omni-channel approaches has revolutionized the way customers interact with lending institutions, allowing for seamless transitions across multiple platforms and devices.

STP vs. N-STP Journeys:

As banks and other financial institutions adjust to the digital age, the ideas of straight pass-through (STP) and near-STP (N-STP) journeys become very important. STP makes it easier to use payment and routing information, so there is no need for manual work during the onboarding process. Sending money used to involve many different departments, which made the process take a long time. STP, on the other hand, speeds up transactions by automating them, which cuts down on processing times by a lot.

But for complicated products and due diligence needs, near-STP (N-STP) journeys may be needed. With N-STP journeys, you can review and check things again to make sure they are correct without slowing things down. By finding the right balance between speed and accuracy, businesses can make the onboarding process better for both customers and themselves. This article will look at how digital transformation and the difference between STP and N-STP journeys are changing the lending landscape. It will also give you an idea of the strategies and technologies that are making this change happen.

Third-Party Entities

Collaboration with third-party agencies and vendors is commonplace in the lending industry, particularly for tasks such as property valuation, legal checks, and personal discussions. In addition to banks or financial institutions (FIs), various external entities play integral roles in the lending journey. These include agencies or vendors contracted by banks/FIs to conduct essential due diligence checks, such as property or collateral valuation, legal assessments, contact point verification (CPV), and personal discussions (PD).

Risk Assessment & Underwriting

The assessment phase is a key part of the lending decision-making process. It uses a lot of information about the customer that was gathered from documents and verification reports. This assessment includes looking at credit and fraud risks, making sure the institution follows the law and rules, and protecting its reputation.

Institutions often use advanced tools like rules engines, AI-based risk scorecards, credit assessment memos (CAM), and credit monitoring arrangements (CMA) to make this process easier. These tools let institutions automate or semi-automate the process of making assessments, which makes them more accurate and efficient.

Sanction & Post-Sanction Process

After the assessment phase, the implementation of sanctions can take many forms, such as digital or workflow-based processes. In banks, authorisation matrices control the sanctioning process by deciding whether approvals are given on an individual basis or through groups like forums or committees.

You can also do post-sanction tasks like signing contracts online or by hand. These tasks include making repayment plans, collecting fees, giving out money, and making charges, among other things. The decision to use digital or manual execution depends on how complicated the transaction is and how good the institution’s technology is.

Key Features of Onboarding Journey Platforms:

Modern onboarding journey platforms offer a plethora of features designed to optimize the customer onboarding experience.

1. Digital and API-first Stack with Microservices-Based Architecture:

These platforms use digital technologies and APIs to make the onboarding process easier, so they can work with a wide range of systems and channels. Microservices architecture lets you break up big applications into smaller, self-contained services. This makes them more flexible, scalable, and easier to maintain!

2. Low Code and Configuration-Powered Platform:

With a low-code approach, schools and businesses can create and customize onboarding journeys with very little coding, which saves time and money on development. Configuration-powered platforms let you customize journeys to meet the needs of your business, which makes it easy to quickly create and test new ideas.

3. Modular Systems Approach

A modular systems approach lets organisations build and deploy onboarding journeys in a modular way, making it easier to scale and work with many different products and lines of business

4. Pre-Integrations and AI/ML/Rules-Based Automation:

Pre-integrated solutions make it possible to connect to external systems and data sources without having to do any manual work. AI, ML, and rules-based automation make processes more efficient and help people make better decisions by automating tasks that are done over and over, looking for patterns in data, and enforcing business rules.

5. Enterprise-Grade Security:

These platforms put security first and use strong measures to protect private customer data and make sure they follow all the rules. Institutions can reduce the risk of data breaches and keep the trust of customers and regulators by using features like encryption, access controls, and audit trails

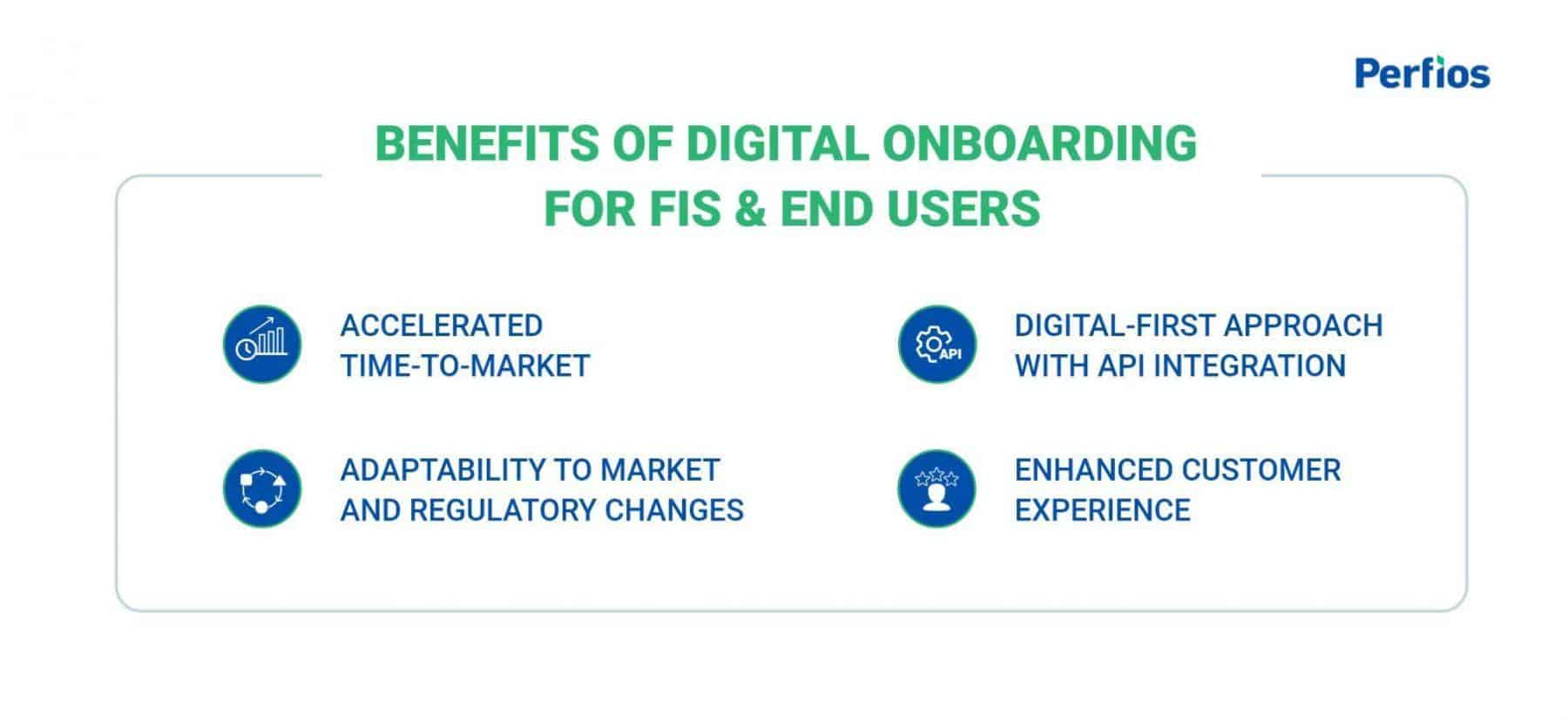

How Digital Onboarding Benefits FIs and End Users?

These are a few ways in which digitization can have an impact on elevating the onboarding experience for FIs and customers:

1. Accelerated Time-to-Market:

Institutions get a competitive edge by shortening the Go-to-Market (GTM) time when they quickly create lending journeys. Institutions can meet changing customer needs and market demands more quickly when they can make product journeys in weeks instead of months.

2. Digital-First Approach with API Integration:

Using a digital and API-first stack makes things more efficient for both banks and financial institutions (FIs) while still giving customers a great experience. Digital validations from trusted sources cut down on processing time and lower the risks and mistakes that come with manual validations.

3. Adaptability to Market and Regulatory Changes:

The platform’s flexibility lets businesses quickly adjust to changes in the market and in the rules. Configurable journeys make it easy to make changes that keep you compliant and competitive in a changing market.

4. Enhanced Customer Experience:

The platform puts the customer experience first by providing an easy-to-use interface with few clicks and the best processing. Auto-filling relevant customer information from digitally verified sources is one of the features that makes the onboarding process easier. It cuts down on manual data entry and makes sure that both end customers and institutions have a smooth experience.

Conclusion:

To change how lenders onboard customers, they need to take a whole-system approach that includes technology, teamwork, and a focus on the customer. By using modern methods and the latest technologies, businesses can make their onboarding processes faster, lower risks, and give customers a better experience overall.

In the end, digital onboarding does more than make operations more efficient; it also gives institutions the tools they need to build stronger relationships with their customers, which leads to loyalty, satisfaction, and growth. As we go through the complicated process of the lending industry’s digital transformation, one thing is clear: the future belongs to those who are open to new ideas and are committed to providing value to both customers and banks.

About InteGREAT:

InteGREAT is a powerful and highly customisable platform for starting, servicing, and managing digital loans from start to finish. It makes sure that it can grow across many Lines of Business (LOBs) and Domains. The platform handles everything automatically, from pre-screening and onboarding to verification, risk and credit review, underwriting, approval, disbursement, and collection.

To know more about how Perfios’ InteGREAT can help your institution scale up and enhance its onboarding practices, please reach out to us at connect@perfios.com