India’s fintech ecosystem, valued at 584 billion in 2022, is projected to reach a staggering 1.5 trillion by 2025, driven by a silent yet powerful force—APIs (Application Programming Interfaces). These digital connectors act as invisible bridges, enabling seamless communication between disparate systems, applications, and platforms. In fintech, APIs empower banks, startups, and businesses to share data, integrate services, and innovate at scale—transforming everything from payments to lending.

India’s rise as a global fintech leader is epitomized by the Unified Payments Interface (UPI), which processes over 16 billion transactions monthly. UPI’s API-driven architecture has democratized digital payments, allowing even street vendors to accept instant, cashless transactions. Beyond UPI, APIs underpin India’s embedded finance boom, where financial services like loans and insurance are integrated into non-financial platforms such as e-commerce and logistics apps. This integration is projected to grow India’s embedded finance market to $28.6 billion by 2029.

With India Stack—a suite of APIs enabling Aadhaar-based authentication, e-KYC, and consent-driven data sharing—the nation has built a world-class digital infrastructure that fuels innovation while ensuring security. As APIs continue to redefine financial inclusivity and efficiency, India is not just participating in the global fintech revolution—it’s leading it.

The Rise of Fintech APIs in India

India Stack: The Backbone of API Innovation

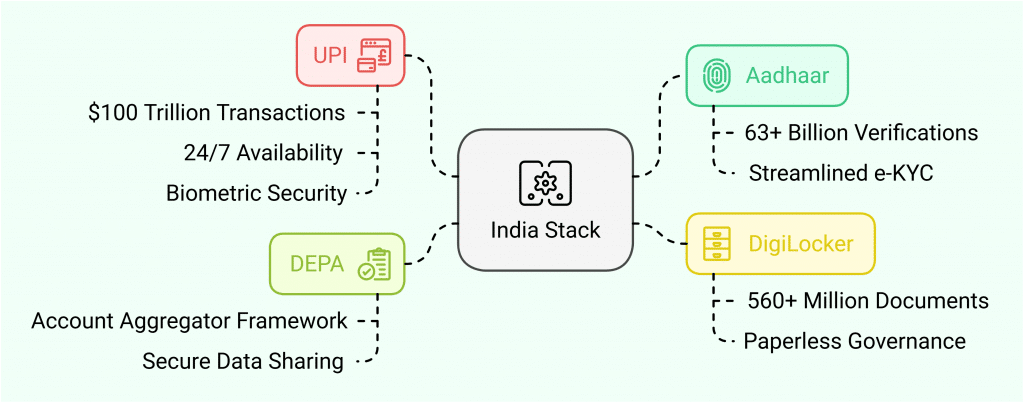

India Stack, a suite of open APIs and digital public goods, has revolutionized financial services through four foundational layers: Aadhaar (digital identity), UPI (payments), DigiLocker (document storage), and DEPA (consent-based data sharing)11. Together, these layers enable secure, interoperable, and scalable solutions:

- Aadhaar has facilitated over 63+ billion digital identity verifications, eliminating physical documentation and streamlining e-KYC processes for millions.

- UPI, the real-time payment rail, processed transactions worth $100 trillion by 2030, driven by its 24/7 availability, biometric security, and merchant ubiquity.

- DigiLocker stores 560+ million digitized documents, reducing fraud and enabling paperless governance.

- DEPA, through the Account Aggregator (AA) framework, allows users to share financial data (e.g., bank statements, tax records) across institutions securely with explicit consent, fostering innovation in lending and wealth management.

This interoperable architecture has positioned India as a global leader in digital infrastructure, enabling startups and enterprises to build inclusive financial products for 1.4 billion people.

Regulatory Catalysts: RBI’s Open Banking Mandates

The Reserve Bank of India (RBI) has been instrumental in accelerating fintech growth through progressive policies:

- The Account Aggregator framework, launched in 2016, has linked 1.1+ billion bank accounts, allowing seamless data sharing between Financial Information Providers (FIPs) and Users (FIUs). This has slashed loan approval times from days to minutes, empowering 112 million users and 2.2 billion financial accounts.

- UPI’s regulatory support transformed it into the world’s largest real-time payment system, processing 16 billion monthly transactions. RBI’s innovations—like UPI Lite for offline transactions and linking credit lines to UPI—ensure accessibility even in low-connectivity regions.

Key Areas Transformed by Fintech APIs

Real-Time Payments and Settlements

Fintech APIs have turned India into a real-time payments powerhouse. The Unified Payments Interface (UPI)—fueled by its open API architecture—processed 131+ billion transactions in FY 2023-24, making it the backbone of India’s cashless economy. From splitting bills at chai stalls to enabling instant salary disbursements for gig workers, UPI’s API-driven interoperability ensures seamless peer-to-peer transfers across 500+ banks and fintech apps. Cross-border innovations are next: the UPI-PayNow linkage with Singapore allows Indian users to send money to Singaporean bank accounts instantly, eliminating hefty forex fees. This API-powered integration is set to expand to 20+ countries, reshaping global remittances.

Financial Inclusion at Scale

APIs are dismantling barriers for India’s underserved populations. Micro-lending platforms leverage alternative credit scoring APIs to analyze non-traditional data—such as telecom usage, utility payments, and social behavior—to offer loans to rural SMEs and gig workers with no formal credit history. For instance, farmers can now secure crop loans within minutes using agritech apps that integrate lending APIs. The Account Aggregator (AA) framework further accelerates inclusion: by enabling secure sharing of financial data (bank statements, tax records) via APIs, loan approvals now take hours instead of weeks, reducing paperwork by 80%. Over 10 million MSMEs have accessed formal credit through these API-driven systems, unlocking $50+ billion in credit flow.

Embedded Finance: Banking Beyond Apps

APIs are embedding financial services into everyday platforms, creating a “banking without banks” revolution. E-commerce apps now offer instant “buy-now-pay-later” loans via lending APIs, while logistics platforms integrate insurance APIs to protect shipments in transit. Agritech apps provide farmers with weather-based crop insurance, and neobanks embed UPI payments into messaging apps like WhatsApp. This API-driven embedded finance market is projected to grow to $28.6 billion by 2029, driven by India’s 800+ million internet users and booming digital commerce.

Enhanced Security and Fraud Prevention

As transactions surge, APIs are fortifying security. AI-driven fraud detection APIs analyze transaction patterns in real-time, flagging suspicious activity (e.g., unusual login locations) and blocking $2+ billion in potential fraud annually. For KYC compliance, APIs instantly verify identities using Aadhaar biometrics and PAN databases, reducing onboarding time from days to seconds. Banks and fintechs also use blockchain-based APIs to create tamper-proof audit trails, ensuring compliance with RBI’s data localization mandates. These innovations have slashed fraud rates by 40% since 2020, building trust in digital finance.

Benefits of API-Driven Financial Services

For Consumers

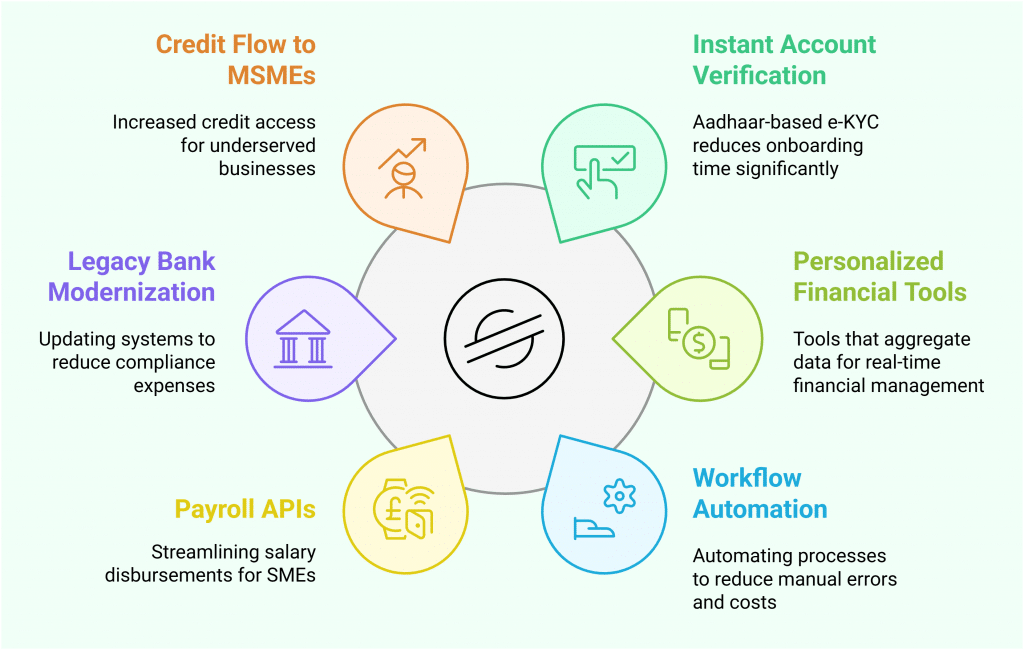

APIs deliver frictionless financial experiences, starting with instant account verification via Aadhaar-based e-KYC, slashing onboarding time from days to seconds. Consumers gain access to personalized financial management tools that aggregate data across banks, enabling real-time budgeting, automated savings, and AI-driven investment advice. For example, apps now alert users about overspending or suggest tax-saving options, empowering 500+ million Indians to make smarter financial decisions effortlessly.

For Businesses

APIs cut operational costs by automating workflows. Invoicing systems integrated with payment gateways process transactions in real-time, reducing manual errors by 70%. Payroll APIs streamline salary disbursements for 10+ million SMEs, saving 30% in administrative costs. Even legacy banks use APIs to modernize infrastructure, trimming compliance expenses by $1.2 billion annually through automated KYC and fraud detection.

For the Economy

API-driven innovation is propelling India’s fintech market toward a 420 billion valuation by 2029. By enabling interoperability, APIs have unlocked 50+ billion in credit flow to underserved MSMEs and fueled a 40% annual growth in digital transactions. This ecosystem supports 5,000+ startups and attracts $10 billion in annual FDI, cementing India’s position as a global fintech leader.

Challenges and Risks

Data Security and Privacy Concerns

While consent-based frameworks like DEPA empower users to control data sharing, breaches in authentication protocols or unauthorized access to Aadhaar/PAN databases pose risks. For instance, phishing attacks targeting UPI users surged by 35% in 2023, highlighting vulnerabilities in API-driven systems. Ensuring end-to-end encryption and real-time monitoring remains critical to prevent identity theft and financial fraud.

Interoperability Gaps

Despite India Stack’s success, fragmented API standards across banks and fintechs create integration hurdles. Smaller institutions often struggle with legacy systems incompatible with UPI’s real-time protocols, leading to delays and errors in payment settlements. Standardizing APIs for cross-platform compatibility is essential to scale innovations like embedded finance.

Regulatory Complexity

The RBI’s stringent data localization rules (mandating Indian servers for financial data) raise operational costs for global fintechs. Frequent updates to cybersecurity guidelines—such as tokenization mandates for card transactions—require constant tech upgrades, burdening startups. Navigating this evolving landscape demands agility, especially for firms leveraging blockchain or cross-border payment APIs.

The Future: APIs Powering Next-Gen Fintech

Voice and IoT-Enabled Payments

APIs are set to revolutionize payments through voice commands and IoT integration. Initiatives like “Hello! UPI” enable voice-based UPI transactions in regional languages, empowering rural users to transfer funds via simple spoken instructions. Wearables like NFC-enabled smartwatches and fitness bands are already facilitating tap-and-pay transactions, with adoption growing among India’s 700 million+ digital payment users. IoT advancements will further automate payments—imagine connected cars paying tolls or smart refrigerators ordering groceries and settling bills autonomously. By 2030, India’s IoT market is projected to exceed $15 billion, driven by APIs that merge financial services with everyday devices.

Sustainability-Driven APIs

Green fintech APIs are aligning finance with India’s climate goals. Platforms now offer APIs for ESG investments, enabling users to fund solar projects or track carbon footprints. For example, APIs integrate with agritech apps to provide loans for eco-friendly farming practices, supporting India’s target of 175 GW renewable energy by 2030. Regulatory frameworks like the Digital Personal Data Protection Act ensure ethical data use, while APIs for green bonds and carbon credits are projected to mobilize $30 billion annually by 2030.

Generative AI Integration

Generative AI is transforming fintech through hyper-personalization. APIs power AI chatbots that resolve queries in regional dialects and analyze spending habits to offer tailored budgeting advice. For instance, lenders use AI-driven APIs to assess creditworthiness using alternative data (e.g., social media activity), expanding access to 40 million thin-file borrowers. However, challenges like AI bias and data privacy require robust governance. By 2030, AI is expected to boost India’s fintech productivity by $200 billion, reshaping everything from fraud detection to wealth management.

Conclusion

APIs have democratized finance, enabling India’s fintech ecosystem to leapfrog traditional barriers and drive its $1.5 trillion vision. From UPI’s real-time payments to the Account Aggregator framework’s inclusive lending, APIs have empowered millions of consumers and businesses alike. As embedded finance, blockchain, and AI redefine financial services, businesses must embrace API-driven models to stay competitive and innovative.

The future is clear: APIs are not just tools but the foundation of India’s digital economy. As one industry leader aptly put it, In the API economy, India isn’t just participating—it’s leading.