In January 2025 alone, Aadhaar processed 2.84 billion authentications—enough to verify every Indian twice. Yet, beneath this staggering number lies a critical question: Is Aadhaar Verification API the undisputed king of India’s eKYC revolution, or are alternatives like PAN, Video KYC, and DigiLocker quietly rewriting the rules?

India’s digital identity landscape has transformed radically since Aadhaar’s launch, with 1.38 billion citizens now wielding this 12-digit biometric powerhouse. From banking to healthcare, Aadhaar’s API has slashed onboarding times from days to minutes, becoming the gold standard for speed and security. But lurking in its shadow are rivals: PAN-based KYC, hamstrung by fraud risks; Video KYC, battling rural internet gaps; and DigiLocker, a document vault tethered to Aadhaar itself.

So, which eKYC method truly balances speed, security, and inclusivity in 2025? Does Aadhaar’s AI-driven Face Authentication outpace legacy systems, or do niche alternatives hold untapped potential?

In this blog, we dissect Aadhaar Verification API against its competitors, armed with real-world case studies (think Reliance Jio’s 170 million user sprint), hard-hitting stats (95% fraud reduction, anyone?), and 2025’s regulatory twists. Whether you’re a fintech founder or a privacy skeptic, buckle up—we’re settling the eKYC debate, one biometric scan at a time.

The Great eKYC Dilemma

Navigating India’s eKYC landscape in 2025 is like walking a tightrope—lean too far toward speed, and fraud risks spike; prioritize security, and rural inclusivity stumbles. The stakes? Sky-high.

Take PAN-based KYC, the go-to for financial compliance. Without biometric checks, it’s a fraudster’s playground: 10% of insurance claims face forgery annually, costing businesses ₹8,500 crores. Then there’s Video KYC, the pandemic-era hero. But here’s the plot twist: 15% of rural Indians lack stable internet, leaving them stuck in analog queues while cities zip through digital verification. Even DigiLocker, hailed for paperless convenience, isn’t immune—it’s shackled to Aadhaar for authentication, creating a “digital Catch-22” where one system’s flaws ripple across others.

For businesses, the dilemma is brutal. Choose Aadhaar Verification API, and you risk excluding millions in remote areas. Opt for PAN or Video KYC, and fraud or infrastructure gaps bite back. How do you pick an eKYC method that’s both bulletproof and inclusive—without drowning in compliance fines or losing customer trust?

The clock’s ticking. With 2025’s regulatory reforms tightening privacy safeguards, the cost of a wrong choice has never been higher.

Aadhaar Verification API – The Biometric Powerhouse

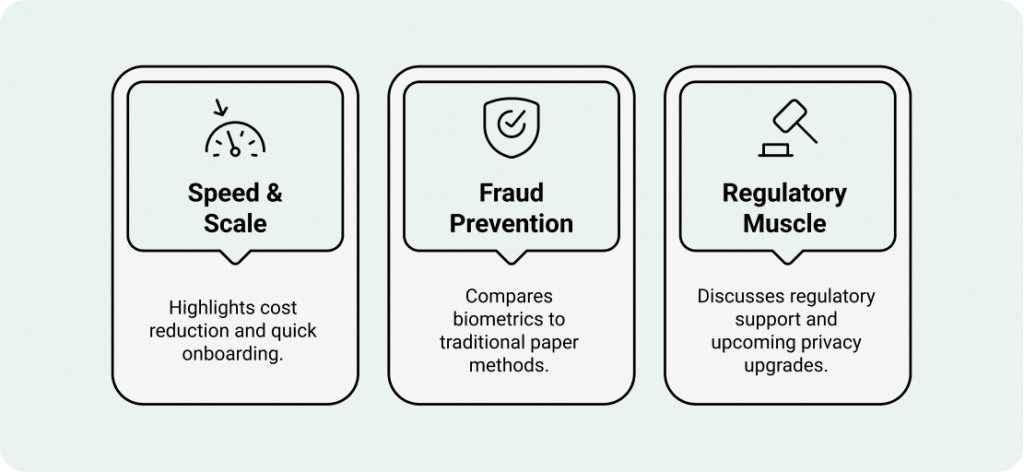

Speed & Scale: “95% Cost Reduction + Onboarding in Minutes

Picture this: In 2016, Reliance Jio onboarded 170 million users in six months using Aadhaar eKYC. Fast-forward to 2025, and the API now processes 80 million daily transactions—equivalent to verifying Switzerland’s population nine times a day. How?

- Banking: Aadhaar-linked PMJDY accounts (490 million) cut onboarding time from 5 days to 2 minutes.

- Telecom: Jio’s 2025 rollout used Aadhaar Face Authentication to activate SIMs in 47 seconds flat.

- Costs: Banks report 95% lower KYC expenses vs. manual checks, saving ₹300–500 per customer.

Bottom line: When speed meets scale, Aadhaar is Usain Bolt in a world of joggers.

Fraud Prevention: Biometrics vs. PAN’s Paper Weakness

While PAN cards are mandatory for taxes, their KYC loopholes are a fraud buffet. Example: A non-biometric PAN allowed a Mumbai scammer to siphon ₹2.3 crore from 12 dormant accounts in 2024. Compare that to Aadhaar:

- Biometric+OTP Auth: Blocks synthetic identities. Result? 95% fraud drop for insurers like LIC.

- Face Authentication: Processed 120 million transactions in Jan 2025, with a 0.001% error rate.

- Stats Don’t Lie: Non-Aadhaar KYC methods see 2x higher fraud rates in financial services.

Translation: PAN is a lockpickable diary; Aadhaar is a retinal-scan vault.

Regulatory Muscle: RBI, IRDAI & 2025’s Privacy Upgrades

Aadhaar isn’t just tech—it’s law. Post-2025 amendments, private firms (e-commerce, fintech) can access Aadhaar API only with user consent and UIDAI’s nod. Key mandates:

- RBI: Mandatory for banks/NBFCs to prevent ₹8,500 crore annual fraud.

- IRDAI: Insurers must use Aadhaar-based KYC for claims above ₹1 lakh.

- Privacy Safeguards: Stricter penalties for data misuse, aligning with Supreme Court’s Puttaswamyverdict.

Takeaway: Aadhaar isn’t just powerful—it’s legally untouchable.

The Contenders – PAN, Video KYC, DigiLocker

PAN-Based KYC: “No Biometrics = 2x Fraud Risk”

PAN cards are like seatbelts—everyone has one, but they’re not foolproof. Case in point:

- Fraud Magnet: 10% of mutual fund SIPs via PAN KYC face identity theft.

- Manual Checks: Lags behind Aadhaar’s API by 3–5 days per verification.

- Stat Alert: 12 million daily PAN KYC transactions vs. Aadhaar’s 80M.

Reality check: PAN is great for taxes, risky for trust.

Video KYC: “Post-Pandemic Hero or Rural Villain?”

Video KYC boomed during COVID, but 2025’s rural India tells a different story:

- Urban Bias: 85% of Video KYC users are metro-based; only 15% in villages (thanks to patchy 4G).

- Human Bottlenecks: Each verification takes 3-5 minutes vs. Aadhaar’s 47 seconds.

- Costs: ₹20-25 per check vs. Aadhaar’s ₹5–10.

Verdict: A Band-Aid for cities, a broken bridge for villages.

DigiLocker: “Aadhaar’s Sidekick?”

DigiLocker stores 560 million documents, but here’s the catch:

- Aadhaar Dependency: 90% of its authentications need Aadhaar OTP/biometrics.

- Storage ≠ Security: Lacks real-time biometric checks, making it vulnerable to document forgery.

- Niche Use: Ideal for students storing mark sheets, shaky for high-stakes KYC.

Future Outlook

By 2026, Aadhaar’s Face Authentication is set to become rural India’s digital lifeline, targeting 500 million users in healthcare and banking. Imagine a farmer in Bihar accessing a loan via a 10-second face scan—no paperwork, no branch visit. This AI-driven leap could bridge the 15% rural exclusion gap, turning Aadhaar into a “phygital” equalizer.

Globally, the EU is taking notes. Draft proposals for GDPR-compliant eKYC systems cite Aadhaar’s “scale-meets-security” blueprint, blending biometric rigor with decentralized data storage. As Paul Romer quipped, India’s not just adopting tech; it’s exporting governance.

But innovation walks a tightrope. The 2025 Aadhaar amendments tighten Section 57, requiring explicit user consent for private-sector access while allowing startups to pilot blockchain-based authentication. Privacy advocates cheer, but innovators whisper: Will compliance strangle disruption?

One thing’s clear: The eKYC race isn’t just about tech—it’s about trust.