Welcome to the world of credit underwriting—a process that’s quietly been undergoing a massive glow-up, thanks to artificial intelligence.

In the evolving world of financial services, credit underwriting remains a cornerstone of lending. Traditionally driven by manual processes and legacy systems, underwriting is now undergoing a quiet revolution that is powered by Artificial Intelligence (AI). This transformation is not just about speed or scale; it’s fundamentally changing how lenders evaluate risk, detect fraud, and make credit decisions.

This blog is the first in a series that explores how AI is reshaping credit underwriting. We will unpack the basics, outline the limitations of conventional methods, and walk through how AI-based solutions such as CreditAssist by Perfios are helping lenders build smarter, faster, and more inclusive credit ecosystems.

What is Credit Underwriting?

Imagine you’re a bank. Your job is to lend money, but not recklessly. You need to know if someone’s likely to pay you back. That’s where credit underwriting comes in.

At its core, credit underwriting is the process by which lenders assess the risk of lending money to a borrower. It involves evaluating a borrower’s financial health, repayment capacity, credit history, and other factors before approving a loan.

For decades, traditional credit underwriting decisions were based on a fixed set of parameters such as credit scores, income proofs, collateral value, and often required manual document checks. While this system worked in the past, it has struggled to keep up with the complexity and speed of modern lending needs, especially in emerging markets.

Challenges in Traditional Credit Underwriting

Despite being fundamental to the lending process, traditional credit underwriting has faced several persistent challenges. Here are some of the biggest pain points:

- Time-Consuming: Manual review of documents and data entry can delay loan approvals, particularly in high-volume credit underwriting environments.

- Limited Visibility: Relying heavily on traditional data like credit scores excludes a large population, especially MSMEs and gig workers, who may not have formal credit histories.

- Subjective Decision-Making: Human bias and inconsistent evaluation standards can result in unfair outcomes and missed opportunities.

- Fraud Risk: Forged documents, identity mismatches and unverified financials can slip through manual credit underwriting reviews.

- Compliance Pressure: Regulatory requirements continue to evolve and ensuring compliance without automation can be both costly and error-prone.

Clearly, there is a need for a more dynamic, scalable, and data-driven approach.

A Quick Look Back: The Evolution of Credit Underwriting

Credit underwriting has come a long way from relying on personal judgments in the 1800s, to using standardised credit scores in the mid-20th century, and now entering the era of AI and machine learning.

To truly appreciate how far we’ve come, let’s rewind the clock!

Imagine it’s the late 1800s. There are no CRIF reports, no CIBIL scores, and certainly no bank statement PDFs. A local banker sits across from a borrower—let’s call him Raj—listening intently to his pitch for a loan to expand his spice business. The banker knows Raj, knows his family, and maybe even buys spices from him at the market. Based on that relationship and a gut feeling, he nods and approves the loan.

This was underwriting in its earliest form: relationship-driven and deeply personal, but wildly inconsistent.

Fast forward to the 1970s. The world of finance begins to formalize. Credit bureaus enter the scene, and so do structured credit scores. Lenders now use more standardized benchmarks like income proof, salary slips, and collateral to make decisions. Underwriting becomes more predictable, but also more exclusive, sidelining those without formal financial footprints.

Then came the 2000s: the age of spreadsheets and rule engines. Banks started automating parts of the underwriting process with software that could apply fixed criteria to loan applications. But here’s the catch: these systems were only as good as the rules they were programmed with. If a borrower didn’t tick all the boxes, the answer was a default “no.”

Now, welcome to the 2020s.

AI and machine learning have entered the chat. We’re no longer talking about just ticking boxes; we’re talking about understanding patterns, analyzing unstructured data, and even predicting borrower behavior. The shift is profound: from rigid, rule-based decisioning to intelligent, adaptive credit underwriting that can flex with each borrower’s unique story.

Think of it like upgrading from a paper map to real-time GPS. Both get you somewhere, but one helps you navigate with nuance.

As we move forward, the question is no longer “Can this borrower repay?” but “What does the full story of this borrower’s financial life look like?” And thanks to AI, we’re now in a position to answer that, faster and more fairly than ever before.

How AI is Changing the Game For Credit Underwriters

AI transforms credit underwriting into a more holistic, objective, and efficient process. Here’s how:

Leveraging Alternate Data for Smarter SME Credit Decisions

Consider a mid-sized logistics firm based in Jaipur with a growing footprint across North India. The company maintains consistent cash flows, has strong vendor relationships, and demonstrates timely statutory compliance. However, due to limited formal credit exposure and a non-standard documentation trail, its profile might appear “thin” to traditional underwriting models.

CreditAssist addresses this gap by intelligently combining traditional financial data with a broad spectrum of alternate data sources including bank statements, GST filings, cash flow patterns, utility bill payments, business registration types, geographic footprint, and digital transaction behavior.

By cross-validating this information, for instance, matching GSTR returns with declared revenue or reconciling vendor payments with cash flow statements, CreditAssist builds a contextual, risk-adjusted credit profile that reflects the business’s actual financial health and operational discipline.

This enables lenders to assess previously overlooked borrowers with greater confidence!

Smart Data Access and Extraction in Credit Underwriting

One of the most time-consuming aspects of underwriting is collecting and parsing data from multiple documents. AI systems can now extract data from PDF bank statements to scanned invoices. With borrower consent, data can be pulled directly from verified sources like Account Aggregators, net banking portals, and GST databases.

This automation drastically reduces manual effort and ensures comprehensive data visibility within minutes.

Comprehensive Financial Analysis

The true value of AI lies not just in data collection but in making sense of the data! AI underwriting tools can auto-calculate financial ratios, track seasonal cash flow patterns, flag anomalies in expense behavior & compare borrower performance against industry benchmarks

Crucially, dashboards can be tailored to meet regulatory and internal credit policies, helping underwriters remain compliant without the hassle.

Data-Driven Credit Underwriting & Decision Making

Once financial analysis is complete, AI systems generate detailed credit reports that provide a 360° view of the borrower. These reports highlight verified income streams, unverified or suspicious transactions, creditworthiness scores, and customized loan recommendations in real-time.

CreditAssist by Perfios: Built for the New Era of Credit Underwriting

At Perfios, we’ve witnessed firsthand how lenders are looking for intelligent systems that can analyse, validate, and decide at scale.

That’s where CreditAssist, our AI-powered underwriting engine, comes in. Built on years of expertise in financial data aggregation, CreditAssist leverages:

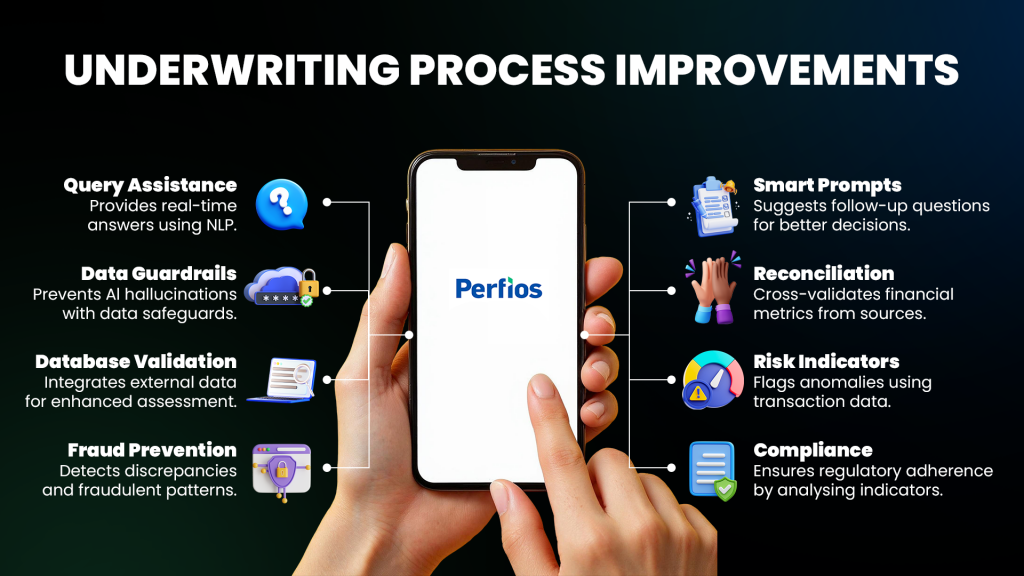

- AI-Powered Query Assistance: Real-time answers to underwriters’ queries using NLP through an interactive 2-way dialogue.

- Smart Query Prompts: Suggests follow-up questions to enhance decision accuracy.

- Data Integrity Guardrails: Prevents hallucinations with built-in data safeguards, keeping AI responses accurate and application-specific

- Multi-Document Reconciliation: Cross-validates financial metrics from various sources for accuracy.

- External Database Validation: Integrates alternate data and open data sources for enhanced assessment with additional cross-validation

- Risk & Strength Indicators: Flags anomalies using transaction and external data analytics to identify key risk factors and strengths

- Fraud Prevention: Detects discrepancies and fraudulent patterns through cross-analysis.

- Regulatory Compliance: Ensures regulatory adherence by thoroughly analysing negative indicators in filing details

Whether you’re a bank underwriting SME loans or an NBFC serving gig workers, CreditAssist helps your credit teams make better decisions faster and with less friction.

Conclusion: Underwriting Shouldn’t Be a Bottleneck!

If your credit teams are still juggling spreadsheets, chasing documents, or second-guessing borrower profiles, something’s broken. In today’s lending landscape, delays, blind spots, and manual errors are lost opportunities.

CreditAssist by Perfios fixes that with clarity offered through automation. We elevate underwriting with intelligent scoring models, configurable policies, and real-time insights that help your credit team make accurate, confident decisions at scale.

You get fewer drop-offs. Smarter approvals. And the peace of knowing your decisions are not grounded in guesswork.

That’s a competitive edge. And that’s what we deliver with CreditAssist.