In 2023, 40% of fintech users abandoned apps mid-onboarding because typing ‘SBIN0005957’ felt like solving a Rubik’s cube blindfolded. Meanwhile, apps using Bank Account Verification API slashed drop-offs by 70%.

Let’s face it: Manual bank verification is the dial-up internet of fintech. Users today want Venmo-smooth experiences, not Excel-sheet uploads that take days and bleed customers. Picture this: A user excited to invest their first ₹5,000—only to quit when your app asks for a scanned bank statement from the last 3 months. Cue the Delete App tap.

Enter Bank Account Verification API—the silent heroes turning this chaos into a 2-minute, one-click miracle. These APIs don’t just validate accounts in real-time; they’re your shield against fraud, compliance headaches, and the dreaded Why is this taking so long?! reviews.

In this guide, we’ll crack open the API integration puzzle—with code snippets (Python/Node.js), cost-slashing hacks (ditch per-check pricing!), and real-world wins (like how CRED onboarded 5M users in 6 months). Whether you’re a startup founder or a CTO at a neo-bank, consider this your playbook to dodge fintech’s biggest buzzkill: clunky verification.

The Verification Vortex

Manual bank verification isn’t just slow—it’s business quicksand. Picture users waiting 3 days for approval while fat-fingering account numbers with a 25% error rate. Each typo isn’t just a delay; it’s a compliance grenade, risking PCI-DSS fines and leaked data. Worse? In 2024, weak verification cost Indian fintechs ₹2,300 crore, with 60% of fraud traced to clunky KYC processes.

But the pain runs deeper:

- User Rage: 40% of customers ditch apps after one verification hiccup.

- Compliance Roulette: Manual checks miss RBI’s KYC updates, inviting audits.

- Fraud Floodgates: Scammers exploit IFSC typos to siphon ₹50 lakh/month from small businesses.

The kicker? While your team drowns in PDF uploads and OTP resets, competitors using Bank Account Verification API onboard users in 2 minutes—with 99.9% accuracy.

So, ask yourself: Is your app one manual error away from becoming the next Data Breach Alert! headline?

Step-by-Step Integration Guide

Choose Your API: Prioritize Coverage, Uptime & RBI Compliance

Start by picking a provider like Perfios that offers:

- Pan-India Coverage: Verify accounts across 150+ banks, including regional rural banks.

- 99.9% Uptime: Critical for handling peak traffic during payday or festival seasons.

- RBA (Reserve Bank of India) Compliance: Built-in adherence to KYC, AML, and data localization norms.

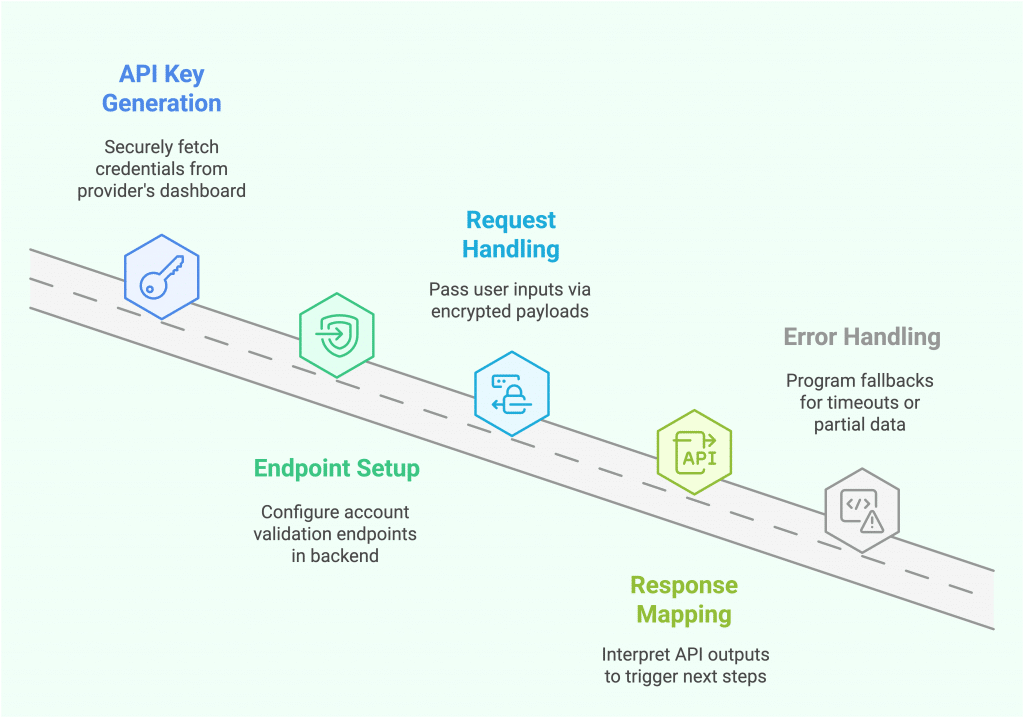

Integration Process

- API Key Generation: Securely fetch credentials from your provider’s dashboard.

- Endpoint Setup: Configure account validation endpoints (e.g.,

/verify-account) in your backend. - Request Handling: Pass user inputs (account number, IFSC) via encrypted payloads.

- Response Mapping: Interpret API outputs (valid/invalid, account holder name match) to trigger next steps.

- Error Handling: Program fallbacks for timeouts or partial data (e.g., Couldn’t verify? Try manual upload).

Testing Hacks: Sandbox Simulations

- Edge Cases: Test invalid IFSC codes (e.g., “SBIN0005958”), closed accounts, or joint holders.

- Load Testing: Simulate 10,000+ concurrent verifications to check latency.

- Compliance Checks: Ensure audit trails auto-capture timestamps, IPs, and consent logs.

Why Bank Account Verification API Is Non-Negotiable

Speed Wins: Cut Onboarding from 72 Hours to 2 Minutes

Manual bank verification is like watching paint dry—slow and painfully outdated. Traditional methods, such as micro-deposits or document uploads, take 3–5 days to confirm account validity. Contrast that with APIs like Teller, which process verifications in seconds by connecting directly to 5,000+ financial institutions 1. For example, Razorpay slashed onboarding times by 80% using real-time APIs, enabling users to start transacting in under 2 minutes 2.

How it works:

- Direct bank integration: APIs bypass intermediaries, validating account numbers and IFSC codes instantly 8.

- Automated workflows: Eliminate manual data entry; APIs auto-fetch and cross-check details like account holder names 9.

- Scalability: Process 10,000+ verifications/hour without breaking a sweat—critical for fintechs handling India’s 1.87 billion daily transactions 9.

Bottom line: APIs turn onboarding from a snail-paced chore into a Formula 1 pit stop.

Fraud Prevention: Detect Mismatches in Real-Time (NPCI’s 2024 Mandate)

Fraudsters love manual verification—it’s their playground. In 2024, NPCI mandated real-time checks for UPI transactions, and APIs deliver. For instance, Softzix’s API flags mismatched account-holder names and IFSC codes before processing payments, reducing fraud risks by 60–80% 34.

Key features:

- Name-IFSC validation: Cross-references account holder names with NPCI databases, blocking impersonators 8.

- Penny Drop Verification: Sends ₹1 to confirm account validity (91% success rate) 4.

- AI-powered anomaly detection: Flags suspicious patterns, like sudden high-value transfers from dormant accounts 7.

Compliance Shield: Automate RBI’s KYC Norms & Audit Trail

RBI’s 2025 updates demand airtight compliance, and manual processes are leaky buckets. APIs like Instantpay auto-generate audit trails for KYC/AML, ensuring every verification is RBI-ready 2.

How APIs ace compliance:

- Auto-recordkeeping: Logs verification timestamps, IP addresses, and user consent 10.

- Regulatory updates: APIs like Smile ID dynamically adapt to new RBI mandates, avoiding fines 7.

- GDPR-ready: Anonymize data post-verification to comply with global privacy laws 4.

Stat alert: Companies using APIs report 30–50% lower compliance costs versus manual audits 11.

Pitfalls to Dodge

Cost Traps: Avoid “Per-Check” Pricing; Negotiate Bulk Deals

APIs save money—unless you fall for predatory pricing. For example, Teller’s “per-check” model charges $1.50 per account verification, which can balloon costs for high-volume apps 1.

Cost-slashing hacks:

- Bulk pricing: Negotiate flat fees (e.g., ₹5–10 per check) with providers like Deepvue 8.

- Hybrid models: Use free tiers for testing (e.g., Teller’s 100 free verifications) before scaling 1.

- Avoid hidden fees: Watch out for charges for failed verifications or API call limits 10.

Security Blunders: Never Store Raw Data; Use Tokenization

Storing raw account numbers is like leaving your house keys under the doormat. APIs like Deepvuereplace sensitive data with tokens, ensuring breaches don’t expose actual account details 8.

Best practices:

- Tokenization: Convert account numbers into irreversible tokens (e.g., “tok_xy12ab”) 10.

- End-to-end encryption: Use APIs compliant with PCI-DSS and ISO 27001 standards 3.

- Regular audits: Test systems quarterly—Perfios.ai recommends simulating phishing attacks to spot vulnerabilities 4.

UX Fails: Add Microcopy Like “Verifying… 37% Faster Than Rivals!”

A silent loading screen is UX kryptonite. Reduce user anxiety with empathetic microcopy:

- Progress updates: Hold tight! We’re verifying your account 2x faster than traditional banks.

- Error handling: Oops! That IFSC code seems off. Let’s try again—we’ll auto-suggest valid options.

ROI Breakdow

| Metric | Manual Verification | API Verification |

|---|---|---|

| Time/Check | 3–5 days | 2–10 seconds |

| Cost/Check | ₹150–200 (labor + errors) | ₹5–10 |

| Fraud Risk | 25% error rate 9 | <1% 4 |

| User Retention | 40% drop-off 2 | 50% higher 4 |

Key Stat: Apps using APIs see 50% higher user retention, as seamless onboarding builds trust 4.

Why This Matters:

- High-volume sectors (e.g., lending, e-commerce) save ₹10+ lakh/month switching to APIs.

- Compliance-heavy industries (insurance, banking) avoid ₹5+ crore in annual fines.

- Startups scale 3x faster with automated workflows.

Future Outlook

By 2026, AI-powered APIs will predict fraud before it happens. Imagine algorithms flagging high-risk accounts (e.g., dormant/closed) during verification, not after. For instance, a user entering an IFSC code linked to a scam-tainted branch could trigger instant red flags—saving fintechs ₹500+ crore annually in preventable fraud.

Globally, India’s API-first model is setting trends. Brazil’s Pix and the EU’s Open Banking Framework now mirror UPI’s real-time, interoperable design, with RBI’s sandbox approach becoming a blueprint for agile regulation.

But the biggest quake? RBI’s 2025 mandate requiring all neo-banks to adopt API-based verification. Non-compliance risks fines up to ₹5 crore/month, pushing even legacy banks to ditch manual checks.

APIs aren’t just tools—they’re the bedrock of a borderless, fraud-proof financial ecosystem. For fintechs, the choice is clear: Integrate or implode.