In the first half of 2023, Indian banks faced 14,483 fraud cases. The culprit? Outdated verification systems. Here’s how APIs are flipping the script.

Picture this: You’re transferring money, but instead of a smooth digital handshake, your transaction relies on a fax machine-era system. That’s the reality for many banks still using manual verification—a sluggish process as risky as leaving your front door wide open. Enter Bank Account Verification API, the tech-savvy guardians of modern finance. These tools act like digital bouncers, instantly validating account details (name, number, branch) during transactions to ensure funds reach the right hands.

The stakes? £1.2 billion lost to UK banking fraud in 2022 alone—enough to buy 6,000 luxury sports cars or fund a small country’s healthcare budget. APIs tackle this by automating checks, slashing errors, and blocking fraudsters faster than a WhatsApp forward goes viral.

In this blog, we’ll unpack how these APIs:

- Turn fraud prevention into a real-time game,

- Save businesses from compliance headaches (and CFOs from stress-eating),

- And deliver wins for companies like Instantpay, who cut fraud by 40%.

Problem Statement: Manual Verification is the Dial-Up Internet of Banking

Imagine trying to stream a 4K movie with dial-up internet. That’s manual bank verification in 2024—slow, glitchy, and utterly frustrating. Here’s why businesses are losing patience:

- Fraud Surge: Scammers are having a field day. Phishing emails, fake accounts, and identity theft drain wallets faster than a kid in a candy store. The UK alone lost £1.2 billion to fraud in 2022—enough to buy 45,000 iPhone 15s or fund a Bollywood blockbuster.

- Manual Errors: Humans are great at creativity, not data entry. A single typo can delay onboarding by 3–5 days—longer than Cheteshwar Pujara’s Test match innings. Worse, 1 in 5 applications get rejected due to avoidable errors, turning customers away like a bouncer at an overbooked club.

- Regulatory Nightmares: Juggling GDPR, RBI guidelines, and cross-border rules is like balancing flaming torches while riding a unicycle. Miss one compliance checkbox? That’s a fine steeper than Everest.

- Legacy Systems: Many banks still run on COBOL code and floppy disk-era tech. Integrating modern APIs? It’s like fitting a Tesla battery into a vintage Ambassador car—possible, but why?

How Bank Account Verification API Work?

Think of these APIs as your bank’s Virat Kohli—reliable, swift, and always on guard. Here’s the playbook:

Real-Time Validation: No More “Penny for Your Thoughts”

- Penny Drop: The API sends a microscopic amount (like ₹1) to the account. If it lands, the account is real. If not? Fraud alert! This method boasts a 91% success rate.

- UPI/IBAN Checks: For instant payments, APIs cross-verify UPI IDs (India) or IBANs (EU) against central databases. It’s like a digital bouncer checking IDs at a club—no fake entries.

- Instant Confirmation: Results in 2–5 seconds, faster than a TikTok trend goes viral.

Open Banking Magic: APIs as the Ultimate Team Players

Thanks to Open Banking, 75% of banks now share data securely via APIs. Imagine a WhatsApp group where banks safely exchange info—no leaks, no drama. This lets businesses verify accounts without storing sensitive data, reducing breach risks like a pro.

Benefits of Using Bank Account Verification API

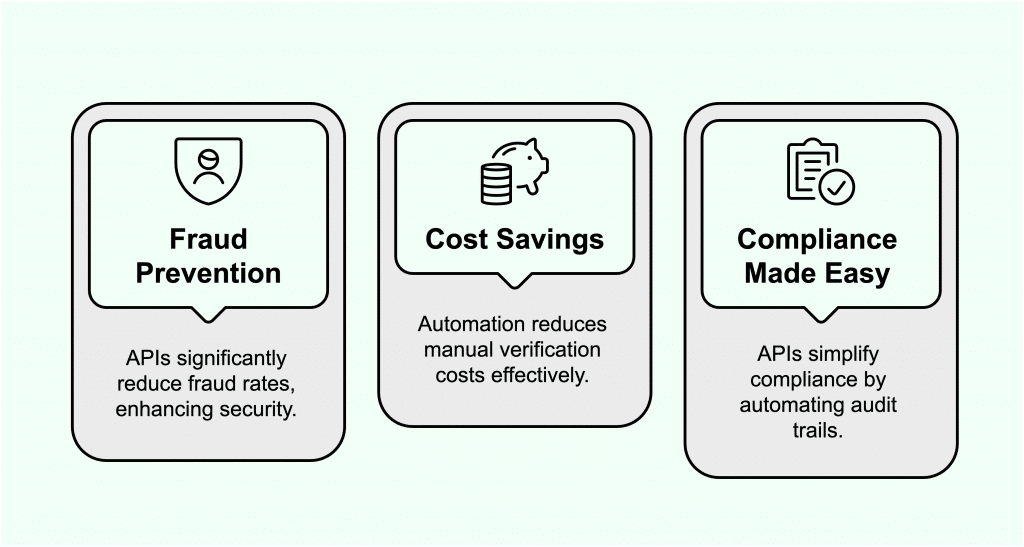

- 1. Fraud Prevention: Block Scams Like a Bouncer: APIs cut fraud by 60–80%, turning businesses into fortresses.

- 2. Cost Savings: CFOs Rejoice!: Automation slashes manual verification costs by 30–50%.

- 3. Compliance Made Easy: Bye-Bye, Spreadsheet Hell: APIs auto-generate audit trails for KYC/AML, keeping RBI and EU regulators happier than fans after a World Cup win.

Challenges to Watch Out For: The Yorker Balls of Tech

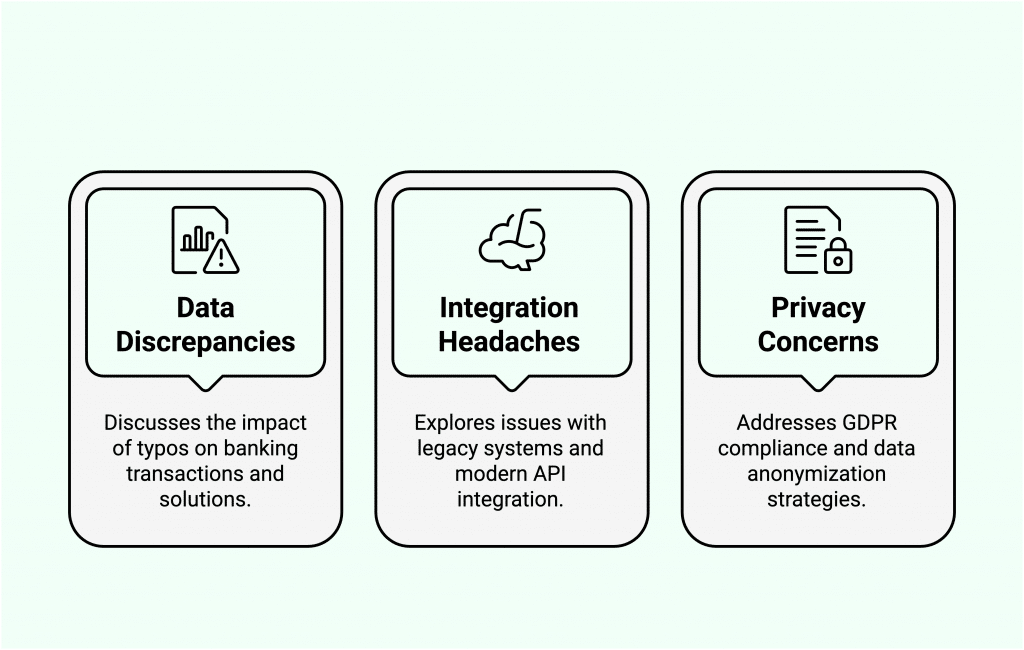

- 1. Data Discrepancies: When Typos Cost Millions: A missing digit or outdated info can trigger “false declines”, annoying customers faster than a dropped Netflix connection. Fix? Use AI to auto-correct inputs—like Grammarly for banking.

- 2. Integration Headaches: COBOL Code vs. Cloud APIs: Legacy systems (read: tech older than SRT’s debut) resist API integration. DIRO cracked this by supporting 44,000+ banks globally—think of it as Google Translate for banking protocols.

- 3. Privacy Concerns: GDPR’s “Right to Be Forgotten”: Balancing security with GDPR’s data deletion rules is trickier than a googly. Solution: Anonymize data post-verification, like shredding sensitive docs after use.

Why This Isn’t a “Set and Forget” Game

Even the best APIs need upkeep:

- Regular Audits: Test systems like a pitch before a match.

- User Education: Teach customers to input accurate details—no more “Goggle” instead of “Google.”

- Hybrid Solutions: Pair APIs with biometric checks for extra security (face scans > passwords).

Banking’s Next Innings—AI, Biometrics & Blockchain

The future of banking security is shaping up to be as exciting as a last-ball T20 finish. Here’s what’s coming in 2025 and beyond:

- AI-Powered Fraud Detection: Algorithms will act like Jasprit Bumrah’s yorkers, flagging suspicious transfers in 0.2 seconds—quicker than you can say “Phishing scam!”

- Biometric Bonanza: Forget passwords. Face scans and fingerprints will become the norm, leaving phishers as outdated as floppy disks. (Pro tip: Hackers might need plastic surgery soon!)

- Blockchain Bridges: Cross-border verification will run on decentralized ledgers, cutting middlemen faster than a third umpire’s decision. DIRO already supports 44,000 banks globally—imagine that scale!

- Quantum-Safe Encryption: With quantum computers looming, banks are prepping encryption that’s tougher to crack than Rahul Dravid’s defense.

In short, banking’s future is sleeker, safer, and way less stressful. Just don’t expect legacy systems to keep up—they’ll be busy collecting digital dust.