Introduction: A Cautionary Tale

Imagine this: A mid-sized regional bank, X, starts 2025 with ambitious plans. After a strong year in 2024, it has expanded aggressively, approving a record number of loans to SMEs and retail borrowers. For months, the strategy seems to pay off with revenues climbing and market share increasing. But by mid-year, cracks begin to show!

Borrowers from the SME sector facing unforeseen economic challenges start missing payments. Retail borrowers follow suit with many unable to manage mounting interest rates. By the third quarter, X’s non-performing assets (NPAs) had doubled. The collections team, overwhelmed by the volume of defaults is struggling to keep up using outdated manual processes.

As legal battles and recovery costs pile up, the bank’s liquidity shrinks. Shareholders demand answers, customers lose trust, and regulatory scrutiny intensifies. By year’s end, X is forced to scale back operations, shelving its growth plans indefinitely.

This story, though fictional, reflects the real challenges banks face worldwide. Bad debts, if unchecked, can derail even the most promising institutions. The key to avoiding such a fate lies in efficient collections systems.

The Ripple Effect of Bad Debts

Bad debts do more than dent profitability; they trigger a cascade of issues that affect every aspect of a bank’s operations.

1. Erosion of Financial Stability

Non-performing loans (NPLs) remain a significant challenge for banks. As of 2023, NPLs represented an average of 4.2% of gross loans globally with some regions like Sub-Saharan Africa seeing rates surpassing 10%.This means billions of dollars tied up in unproductive assets. Such high levels of bad debts strain financial stability, locking up funds that could otherwise fuel lending and economic growth.

2. Operational Strain

Managing bad debts is labor-intensive and costly. The European Central Bank highlighted that debt recovery costs for financial institutions often exceed 10% of their operational budgets. Consider this: the average bank spends 10–15% of its operational budget on debt recovery, including legal fees, collection agent commissions and administrative overhead. These costs eat into already narrow margins.

3. Customer and Reputational Fallout

Aggressive debt recovery methods not only alienate existing customers but can also tarnish a bank’s public image. In an era of heightened customer sensitivity and social media influence, such reputational risks can have long-lasting consequences.

The Hidden Costs: Beyond the Surface

The real damage of bad debts often lies in their less visible but equally harmful consequences.

1. Capital Opportunity Costs

Every rupee locked in non-performing assets is a rupee that cannot be lent to creditworthy customers. For instance, banks with high NPAs have limited capacity to invest in emerging sectors like green finance or digital transformation.

2. Stricter Regulatory Pressures

In India, regulatory tightening around bad debts and non-performing assets (NPAs) is a significant factor stressing the banking sector. The Reserve Bank of India (RBI) has implemented various measures to streamline asset quality and enforce stricter provisioning norms.

For instance, in 2023, the RBI revised provisioning requirements for urban cooperative banks. Tier I UCBs were directed to increase provisioning for standard assets from 0.25% to 0.4% with compliance deadlines extended to March 2025. Furthermore, the RBI issued guidelines in June 2023 harmonizing compromise settlements and technical write-offs, emphasizing transparency and stricter oversight in cases involving defaulters. Regulatory provisions also continue to prioritize early identification of stressed accounts through frameworks like the Special Mention Account (SMA) classification, ensuring prompt remedial actions to prevent defaults from escalating into NPAs.

These measures echo the global trend of enhanced regulatory scrutiny, demanding banks invest heavily in compliance infrastructure and efficient debt recovery mechanisms to meet these expectations. In India, this focus aligns with the broader objective of maintaining financial stability while navigating the complexities of increasing credit demand and potential asset quality risks.

3. Employee Burnout

Collections staff often face the most challenging aspects of bad debt management. Their role involves endless cycles of contacting defaulters, navigating difficult negotiations and managing disputes; all of which can take a heavy toll on morale. For instance, consider a collections team at a mid-sized bank managing a portfolio with rising NPLs. With thousands of overdue accounts, staff members must make repeated calls, often dealing with unresponsive or agitated borrowers. These interactions can lead to emotional exhaustion, frustration and burnout.

Such conditions contribute to high attrition rates in collections teams compounding operational inefficiencies. As experienced employees leave, the organization must continually train replacements, impacting continuity and overall performance.

Why Efficient Collections Systems Are Non-Negotiable in 2025

As the global financial ecosystem grows more complex, the traditional “one-size-fits-all” approach to collections no longer works. Banks need dynamic and adaptable systems. Here’s why:

1. The Rise of Diverse Borrower Profiles

Borrowers today span a wide spectrum, from tech-savvy millennials to struggling SMEs. Each group requires a different engagement strategy. A robust system can segment borrowers and apply tailored solutions, improving outcomes.

2. Mounting Economic Uncertainties

With economic growth slowing in several regions, delinquencies are expected to rise. Advanced systems equipped with predictive analytics can flag high-risk accounts early, enabling pre-emptive action.

3. Competitive Pressures

In a crowded market, banks cannot afford inefficiency. McKinsey reports that banks with automated collections systems recover debts 30% faster and at a 25% lower cost than their peers.

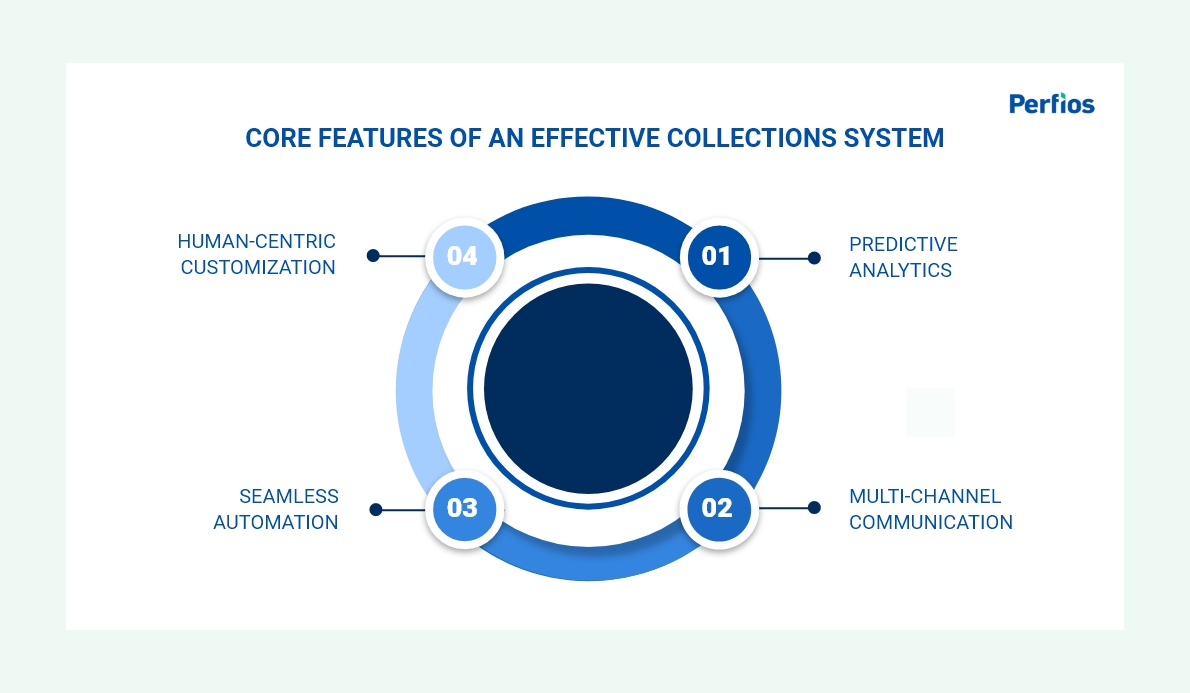

Core Features of an Effective Collections System

To address bad debts effectively, banks must deploy systems that combine technology, strategy, and empathy.

1. Predictive Analytics

These tools analyze borrower behavior to identify delinquency risks early. For example, a system might flag a customer who has missed two consecutive utility payments, allowing the bank to engage proactively.

2. Multi-Channel Communication

An efficient system connects with borrowers where they are via SMS, email, app notifications or even WhatsApp.

3. Seamless Automation

From automated reminders to scheduling repayment plans, automation minimizes delays and reduces errors. Solutions like Perfios Garner enable real-time monitoring of account activity, ensuring swift responses to missed payments.

4. Human-Centric Customization

While technology drives efficiency, human interaction remains vital especially for distressed borrowers. Offering debt restructuring options or counseling services can significantly boost recovery rates and preserve customer relationships.

Actionable Steps for Banks To Reduce Bad Debts:

Banks can tackle bad debts head-on by implementing these strategies:

1. Embrace Technology

Adopt AI, machine learning and automation to streamline recovery workflows and enhance accuracy.

2. Train Staff in Empathy

Equip teams with soft skills to handle sensitive conversations, ensuring respectful and effective engagement.

3. Collaborate with Fintechs

Partner with technology providers specializing in debt management to access state-of-the-art tools and expertise.

4. Monitor and Adapt

Use data insights to continuously refine collections strategies, adapting to changing borrower behaviors.

Conclusion: The Path Forward

The cost of bad debts isn’t just monetary; it’s a systemic issue that affects liquidity, customer trust, and long-term growth. In 2025, the stakes are higher than ever. Economic uncertainty, evolving regulations and rising borrower expectations demand that banks rethink their approach to debt recovery. By investing in advanced tools, adopting empathetic strategies, and fostering agility, banks can turn the tide on bad debts, ensuring resilience and growth in an ever-changing financial landscape.

The future belongs to banks that act decisively today. Will yours be one of them?