Introduction:

The banking industry has changed since the global pandemic. This is because customers’ needs have changed and banks need to keep up with a world that is quickly becoming more digital. As more and more people want personalised, safe, and digital solutions, traditional banks need to quickly change how they do business to meet the changing needs of their customers. The onboarding process is now more important than ever in the lending process. It is the key to building long-lasting relationships with customers and making sure lenders trust and believe in you from the start.

Non-Banking Financial Companies (NBFCs) and Fintechs have become very popular in the lending world today, especially with younger borrowers. NBFCs are appealing because their advanced technology and streamlined processes make things go quickly and easily. NBFCs offer personalised loan options for personal and small business financing needs, unlike traditional banks, which have a lot of paperwork and long processes. Recent studies show that people prefer NBFCs because they are easier to use and more efficient, even though there may be some downsides, such as higher interest rates and worries about data security.

Young people, in particular, like NBFCs because they are quick and easy to use. This is part of a larger change in what consumers want. NBFCs are great at meeting the changing needs of borrowers in today’s fast-paced world because they don’t need a lot of paperwork and can process loans quickly. But even though borrowing from NBFCs is now common, there are still problems that make the lending process difficult.

Why do lenders need a seamless onboarding process?

In the lending business, it’s important to have a smooth and easy onboarding process in order to build long-term relationships with customers. Not only does it set the tone for the customer’s relationship with the lender, but it also lays the groundwork for making effective decisions and judging risk later on.

Why loan onboarding breaks today (and what lenders lose)

Nowadays, loan onboarding should do more than just gather information about customers. It needs to check people’s identities, make sure they follow the rules, accurately assess risk, and give borrowers a smooth experience, all in real time. But for many lenders, onboarding is still one of the weakest links in the lending value chain.

System fragmentation is a big reason why onboarding fails. KYC, credit checks, bank statement analysis, decision-making, and record-keeping are often done with tools and vendors that don’t talk to each other. This means that data has to be entered over and over again, handed off by hand, and the results are different on different channels. These problems get worse as more applications come in.

Another problem is that people depend too much on manual processes. When people are involved in checking data, handling exceptions, and checking documents, it takes longer and makes mistakes. It’s also hard to scale up without raising operational costs by the same amount when you do manual reviews.

The problem is made worse by the fact that regulations are so complicated. Because KYC rules, consent frameworks, and audit requirements change often, lenders have to keep changing their onboarding processes. Without compliance controls that can be set up and run automatically, teams have to use workarounds that slow down processing and make things riskier.

Lenders lose more than just speed when onboarding breaks. They see more borrowers dropping out before they get approved.

- The cost per loan goes up because of rework and manual labour.

- Not being able to see borrower’s risk early on in the process

- More likely to be a victim of fraud or fail to follow rules

In a lending market with a lot of competition, these losses have a direct effect on growth, profits, and customer trust.

5 Ways a Poor Onboarding Process Can Impact Lenders:

1. Increased Drop-Off Rates: Non-compliance, a cumbersome user experience and data inadequacy in the onboarding process can lead to frustration among customers, resulting in higher drop-off rates.

2. Hindered Decision-Making: Inadequate data collection and compliance failures during onboarding can impede lenders’ ability to gather essential information to assess the borrowers’ creditworthiness for informed decision-making.

3. Elevated Risk Levels: Poor onboarding practices & inadequate KYC measures can contribute to elevated risk levels for lenders leaving them susceptible to fraudulent activities and financial crimes.

4. Diminished Trust and Confidence: A subpar onboarding experience can erode trust and confidence in lenders, undermining the credibility of the institution in the eyes of potential borrowers.

5. Operational Inefficiencies: Cumbersome workflows and manual interventions can hamper operational efficiency, impacting the overall productivity and agility of the lending institution.

STP vs N-STP onboarding (how INTEGreat supports both)

Straight-Through Processing (STP) has become a key goal for modern lenders. In an ideal STP journey, a borrower’s application flows from initiation to decision and approval with minimal or no manual intervention. This is especially effective for high-volume, low-risk products such as personal loans, consumer durable financing, or small-ticket business loans.

However, not all loan journeys can be fully STP. Complex borrower profiles, higher ticket sizes, thin-file customers, or regulatory exceptions often require manual review, additional documentation, or assisted decisioning. This is where Non-STP (N-STP) workflows remain essential.

The challenge for lenders is not choosing between STP and N-STP, but supporting both within a single onboarding framework. INTEGreat is designed with this dual reality in mind. The platform enables:

- Fully digital, STP-driven onboarding journeys where data is available, risk is low, and rules are clearly defined

- Assisted and exception-based N-STP journeys where human oversight, additional checks, or customised underwriting is required

By combining automated data ingestion, configurable business rules, and human-in-the-loop workflows, INTEGreat allows lenders to maximise STP rates without sacrificing control or compliance. This ensures operational efficiency at scale while retaining the flexibility needed for real-world lending scenarios.

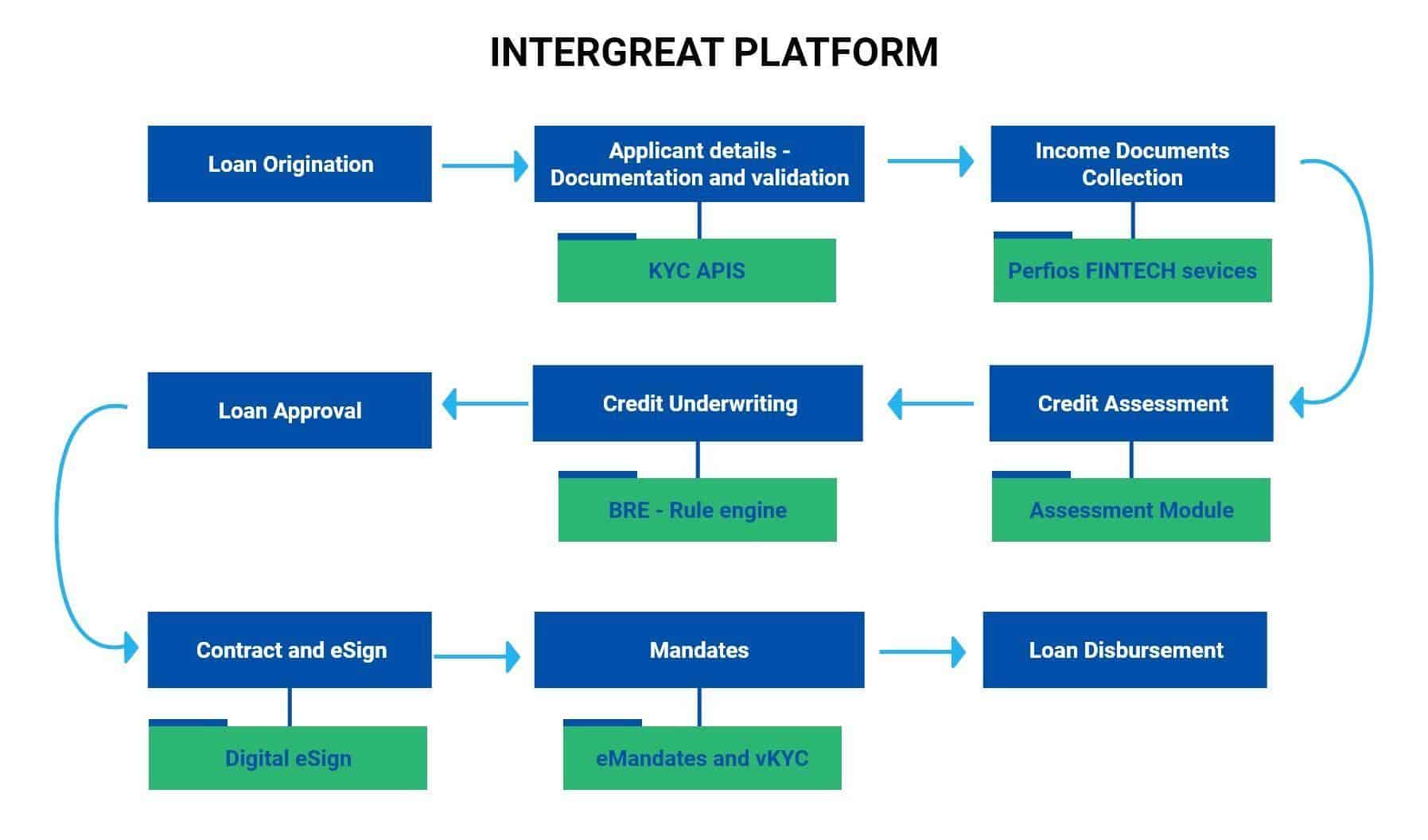

How Does Perfios’ INTEGreat Platform Revolutionize Loan Onboarding?

Our groundbreaking loan onboarding platform, INTEGREAT, exemplifies a revolution in banking. With minimal data input, banks can seamlessly onboard loan customers with the platform’s integrated KYC APIs. This integration works by ensuring seamless onboarding & verification, drastically reducing the time-to-approval (TAT) for loan applications. Moreover, InteGREAT’s automation streamlines application fulfillment, minimizes manual errors and expedites the entire credit process.

InteGREAT makes things easy for customers by giving them a streamlined experience that makes it simple to get loan approvals. Read on to learn how lenders can use the platform’s advanced features to make the onboarding process for their customers smooth:

1. Instant KYC Verification: Perfios’ INTEGreat platform streamlines KYC verification through Perfios KYC APIs, ensuring instant verification and reducing turnaround time (TAT) for loan applications.

2. Automated Credit Process: The entire credit process is automated, minimizing manual effort and errors associated with traditional onboarding methods.

3. AI-Driven Credit Processing: Utilizing advanced AI-driven algorithms, InteGREAT conducts automated bank statement analysis, EPF assessment, cash flow analysis, and VAT/Credit bureau reports & transforms credit processing.

4. Data-Driven Decision-Making: Leveraging Perfios, APIs, InteGREAT enables data-driven decision-making, allowing for better risk assessments, early detection of red flags, and gathering of customer inputs for improved risk mitigation strategies.

5. Decisioning Business Rule Engine (BRE): Our Decisioning Rule Engine (BRE) enables large banks to automate product-related business rules, facilitating faster and more effective decision-making processes.

6. Curated Credit Scoring: InteGREAT provides lenders with product-level credit scoring for a complete picture of borrowers’ financial history for better credit decision-making capabilities.

7. Robust Credit Underwriting: We provide assessment modules for product and loan ticket sizes ensure robust credit underwriting, optimizing risk management and lending practices.

8. Pre-Integrated Digital e-Sign and v-KYC: InteGREAT offers pre-integrated digital e-signature and video KYC capabilities, expediting the application process for a seamless digital customer journey

9. Streamlined End-Customer Journey: With InteGREAT, customers benefit from a streamlined and frictionless experience, available both as a direct customer journey and through an assisted journey within the platform. The platform’s auto form fill feature, coupled with built-in BRE and assessment tools ensures a seamless experience in getting loans sanctioned.

10. Hyper-Personalized Analytics: InteGREAT leverages analytics for targeted marketing purposes through hyper-personalization. By analyzing customers’ transaction histories, online behavior, demographics, and more, the platform enables lenders to tailor their offerings to individual preferences and needs.

How does InteGREAT impact ROI?

1. Streamlined Loan Processing: Moving to a paperless, simpler, and digitised loan processing cycle makes the workflow more efficient.

2. Flexible Deployment Options: Our product works with both Oncloud and on-Premise solutions, so it can be tailored to fit the needs and infrastructure of your business.

3. Improved Workflow: Well-organised application processing and AI-based credit analysis help both banks and borrowers save time and money by speeding up approvals and lowering overhead costs.

4. 360-Degree Application View: Each application gets a full picture thanks to built-in automated checks of the customer’s identity, credit, and bank statements.

5. Consistency and Compliance: Rule-based credit decisioning makes sure that decisions are fair and that rules are followed more closely.

6. Better User Experience: A user interface that is both attractive and easy to use makes it easier for customers to navigate, which speeds up the signup process and increases customer satisfaction and retention rates.

7. Centralised Information Management: A system that is both centralised and integrated makes it easy to collect and access information at any time and from any location.Conclusion: Embracing the Future

Conclusion: Embracing the Future

The InteGREAT platform from Perfios marks a turning point in the history of loan onboarding. By using the latest technology and putting the customer first, it has changed the way banks and borrowers interact with each other. There are many possibilities for the future of loan onboarding. As new technologies like blockchain and predictive analytics get better, banks and other financial institutions will have even better tools for making decisions and assessing risk. There is no limit to the new ideas that can come from personalised lending solutions. This means that loans will not only be products, but also unique experiences.

You can talk to our team to learn more about the product and not miss out on the big wave in loan onboarding technology.

About Perfios:

Perfios Software Solutions is India’s largest SaaS-based B2B fintech software company enabling 1000+ FIs to take informed decisions in real-time. Headquartered in mumbai, India, Perfios specializes in real-time credit decisioning, analytics, onboarding automation, due diligence, monitoring, litigation automation, and more.

Perfios’ core data platform has been built to aggregate and analyze both structured and unstructured data and provide vertical solutions combining both consented and public data for the BFSI space catering to their stringent Scale Performance, Security, and other SLA requirements.

You can write to us at [email protected]

For more Such information contact us@ https://solutions.perfios.com/request-for-demo